values = _utils.download_returns('SPY', '5y')

snapshot(values)

to_plotly (fig)

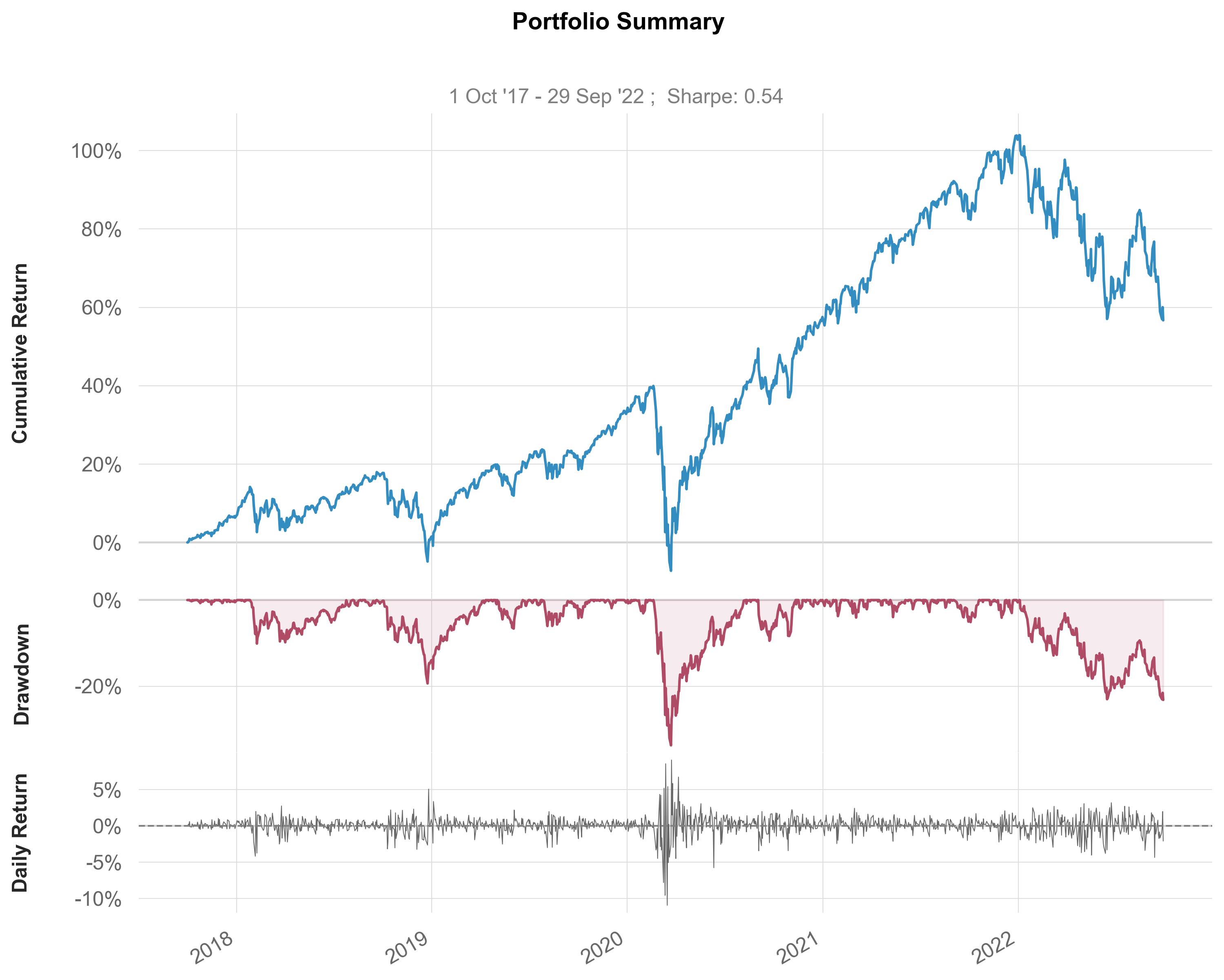

snapshot (returns, grayscale=False, figsize=(10, 8), title='Portfolio Summary', fontname='Arial', lw=1.5, mode='comp', subtitle=True, savefig=None, show=True, log_scale=False)

values = _utils.download_returns('SPY', '5y')

snapshot(values)

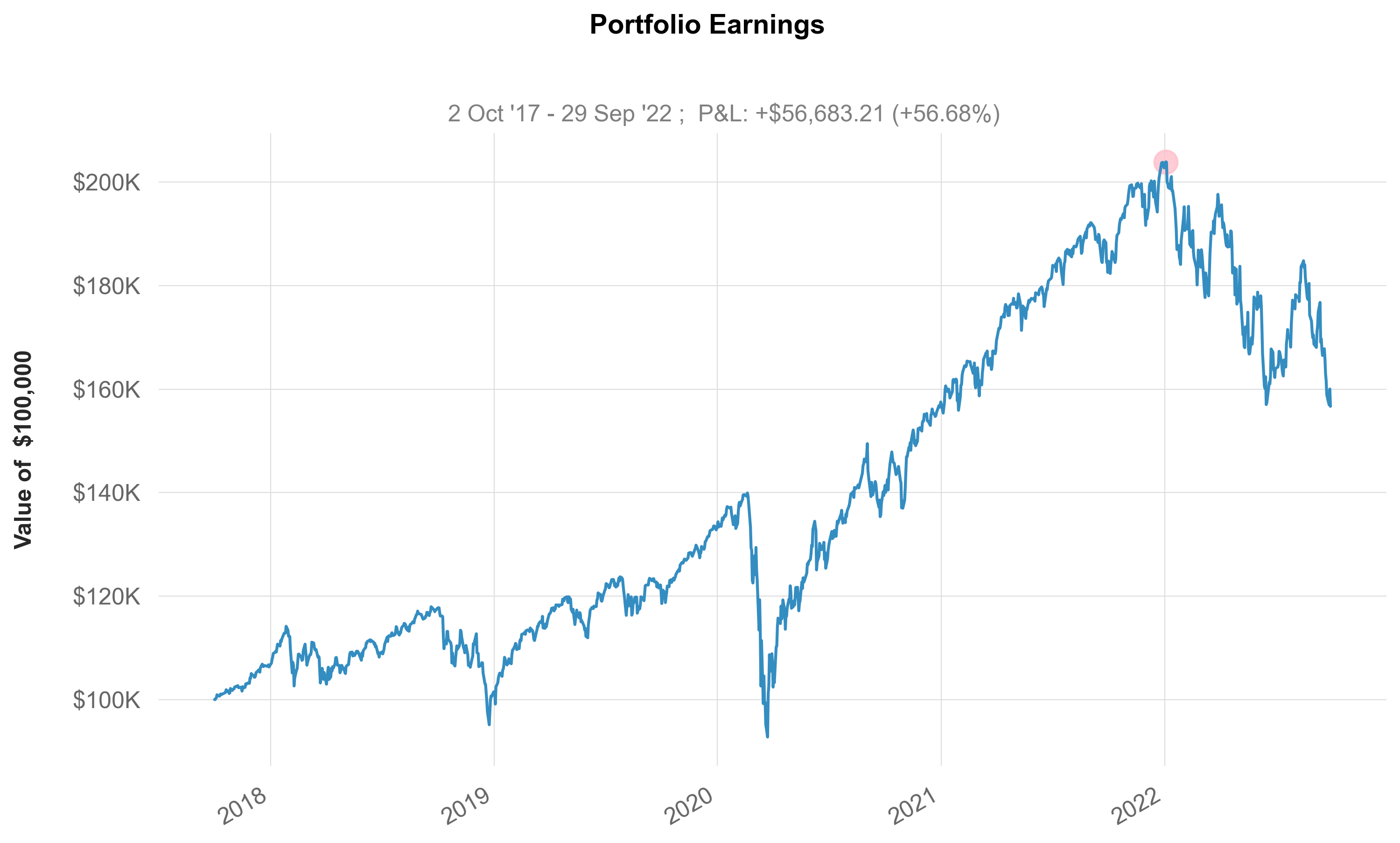

earnings (returns, start_balance=100000.0, mode='comp', grayscale=False, figsize=(10, 6), title='Portfolio Earnings', fontname='Arial', lw=1.5, subtitle=True, savefig=None, show=True)

values = _utils.download_returns('SPY', '5y')

earnings(values)

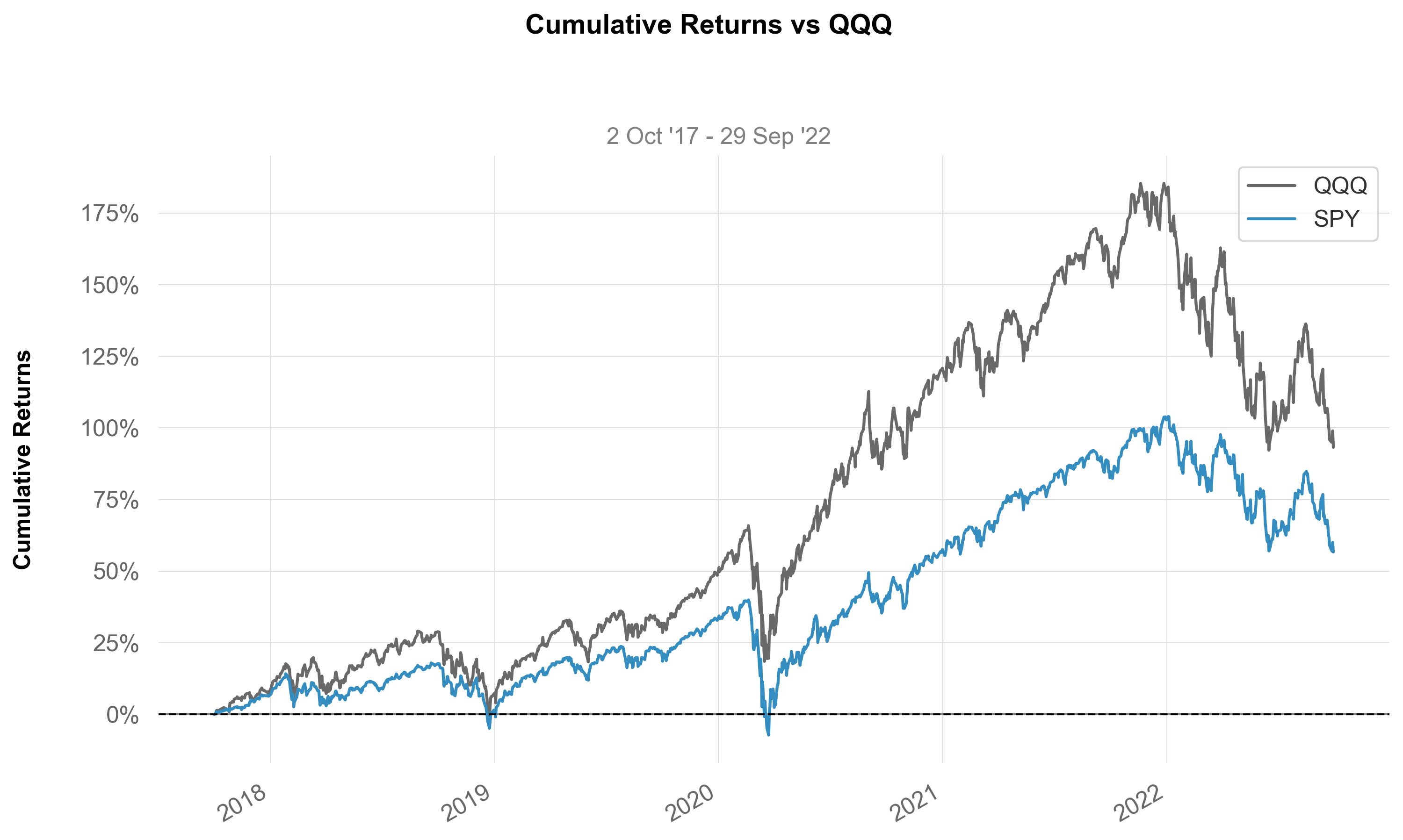

returns (returns, benchmark=None, grayscale=False, figsize=(10, 6), returns_label='Strategy', benchmark_label='Benchmark', fontname='Arial', lw=1.5, match_volatility=False, compound=True, cumulative=True, resample=None, ylabel='Cumulative Returns', subtitle=True, savefig=None, show=True, prepare_returns=False)

values = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

returns(values, benchmark, returns_label="SPY", benchmark_label="QQQ")

daily_returns (returns, grayscale=False, figsize=(10, 4), fontname='Arial', lw=0.5, log_scale=False, ylabel='Returns', subtitle=True, savefig=None, show=True, prepare_returns=True)

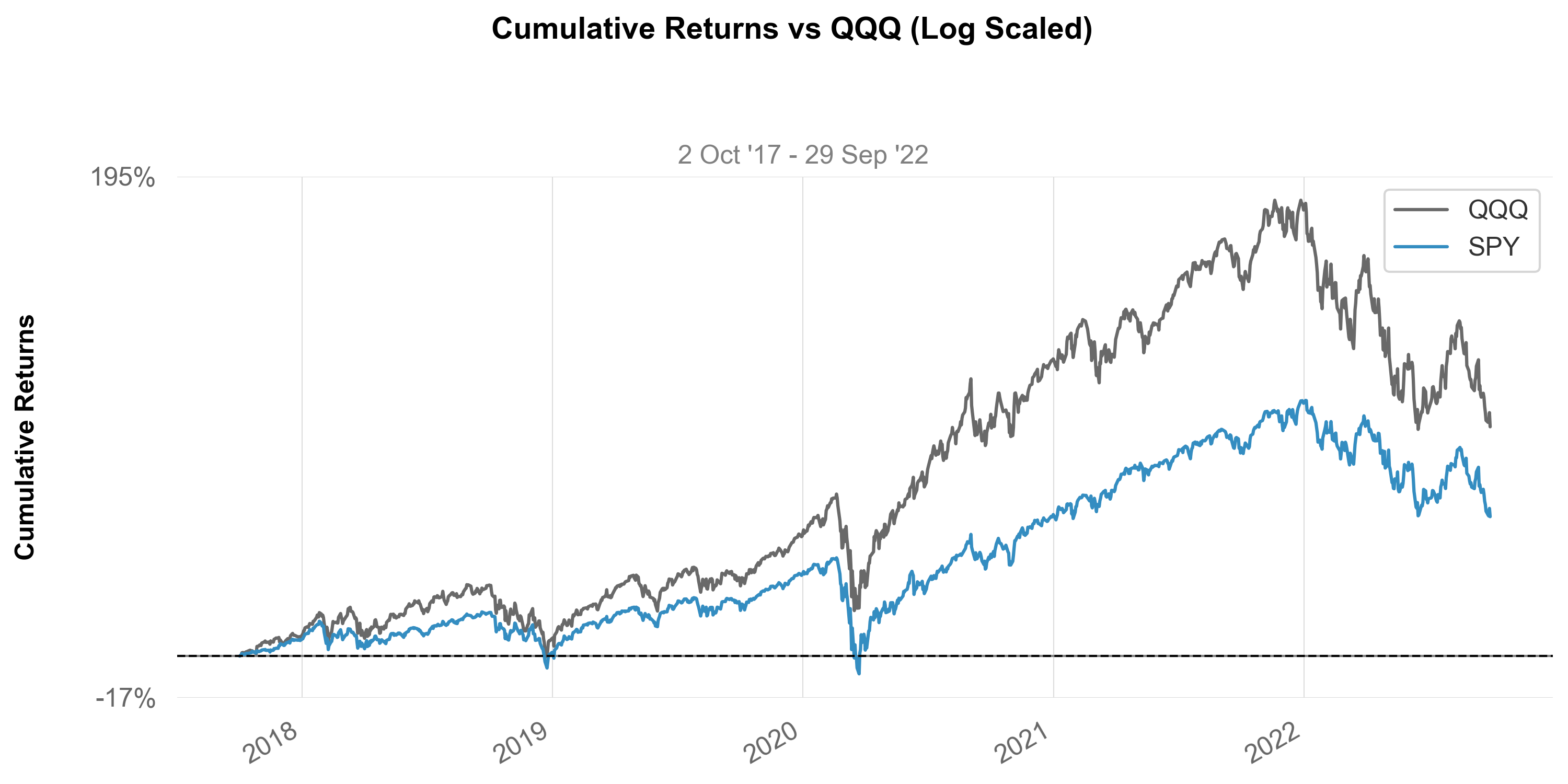

log_returns (returns, benchmark=None, grayscale=False, figsize=(10, 5), returns_label='Strategy', benchmark_label='Benchmark', fontname='Arial', lw=1.5, match_volatility=False, compound=True, cumulative=True, resample=None, ylabel='Cumulative Returns', subtitle=True, savefig=None, show=True, prepare_returns=False)

values = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

log_returns(values, benchmark, returns_label="SPY", benchmark_label="QQQ")

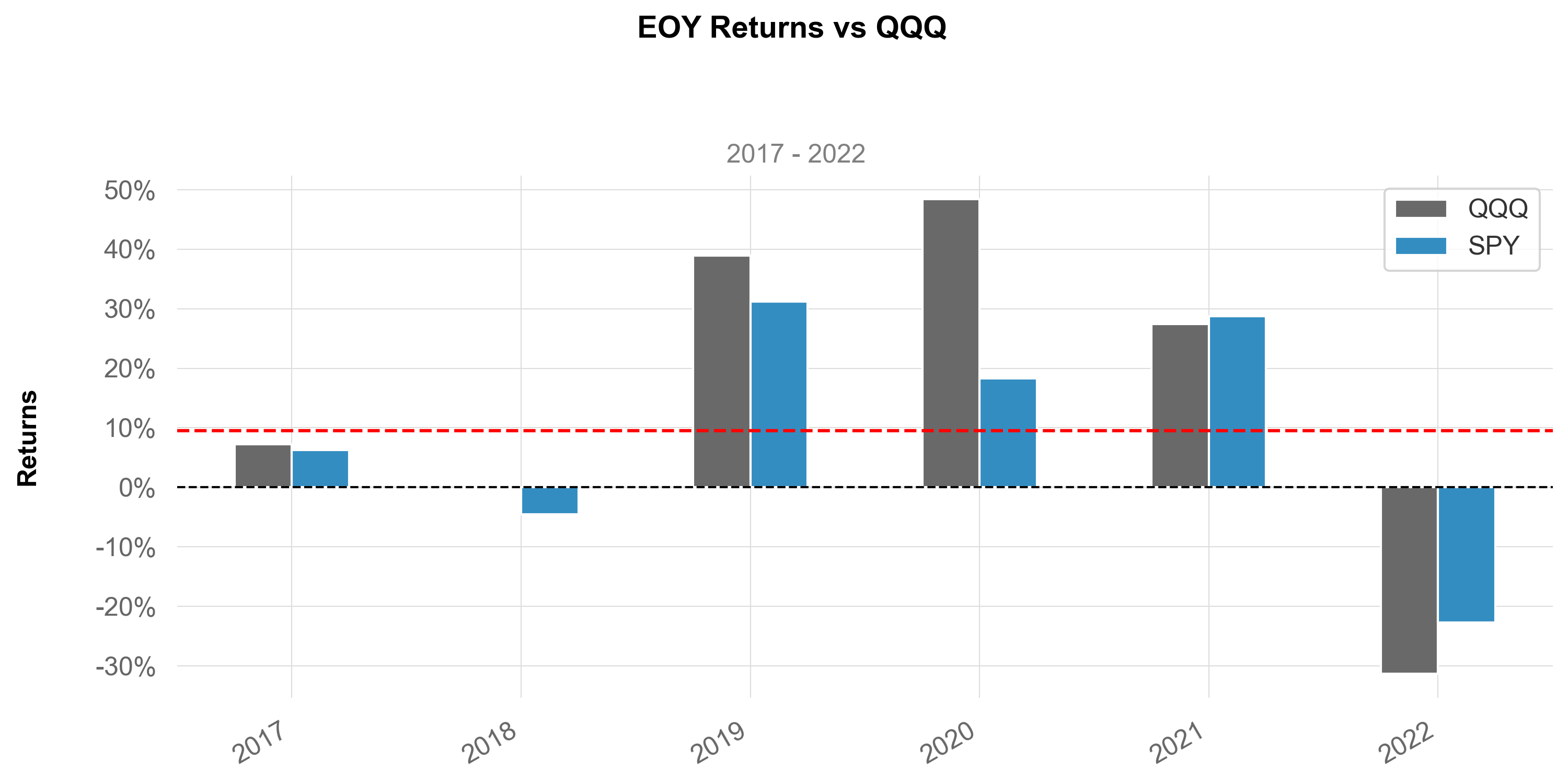

yearly_returns (returns, benchmark=None, returns_label='Strategy', benchmark_label='Benchmark', fontname='Arial', grayscale=False, hlw=1.5, hlcolor='red', hllabel='', match_volatility=False, log_scale=False, figsize=(10, 5), ylabel=True, subtitle=True, compounded=True, savefig=None, show=True, prepare_returns=True)

values = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

yearly_returns(values, benchmark, returns_label="SPY", benchmark_label="QQQ")

distribution (returns, fontname='Arial', grayscale=False, ylabel=True, figsize=(10, 6), subtitle=True, compounded=True, savefig=None, show=True, prepare_returns=True)

values = _utils.download_returns('SPY', '5y')

distribution(values)

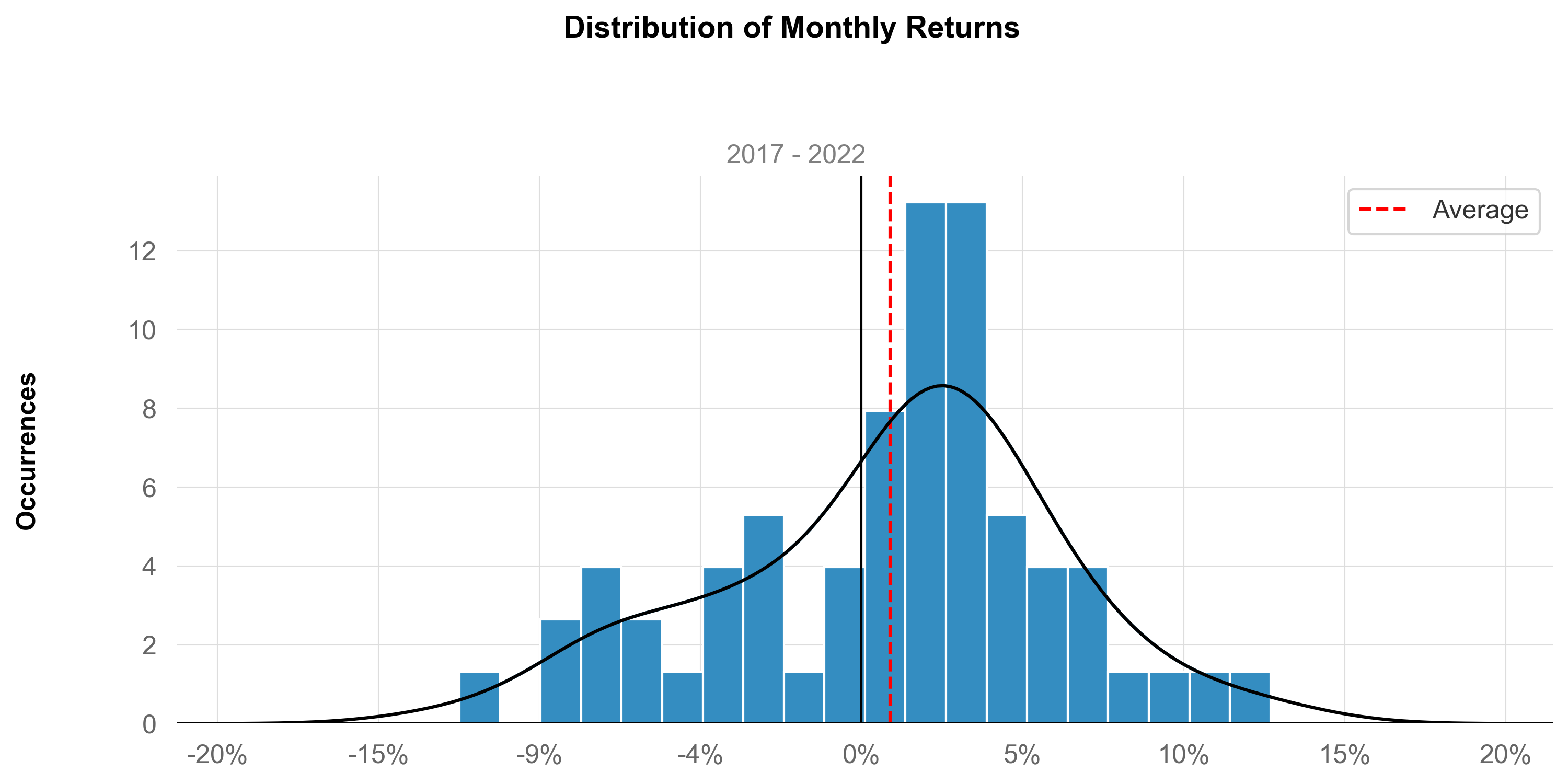

histogram (returns, resample='M', fontname='Arial', grayscale=False, figsize=(10, 5), ylabel=True, subtitle=True, compounded=True, savefig=None, show=True, prepare_returns=True)

values = _utils.download_returns('SPY', '5y')

histogram(values)

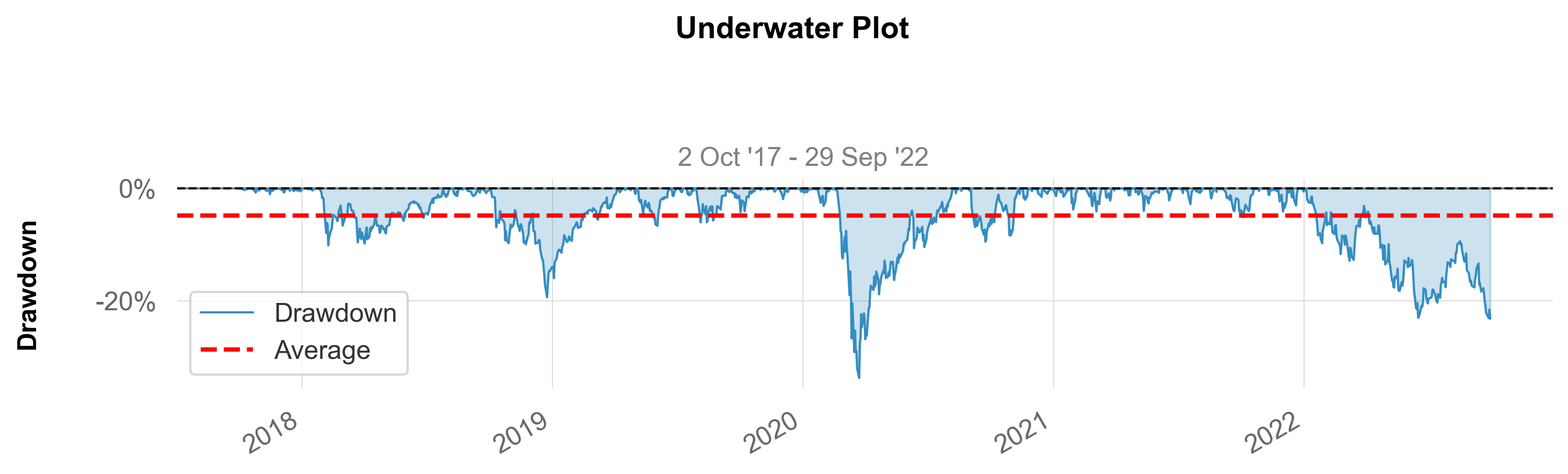

drawdown (returns, grayscale=False, figsize=(10, 3), fontname='Arial', lw=1, log_scale=False, match_volatility=False, compound=False, ylabel='Drawdown', resample=None, subtitle=True, savefig=None, show=True)

values = _utils.download_returns('SPY', '5y')

drawdown(values)

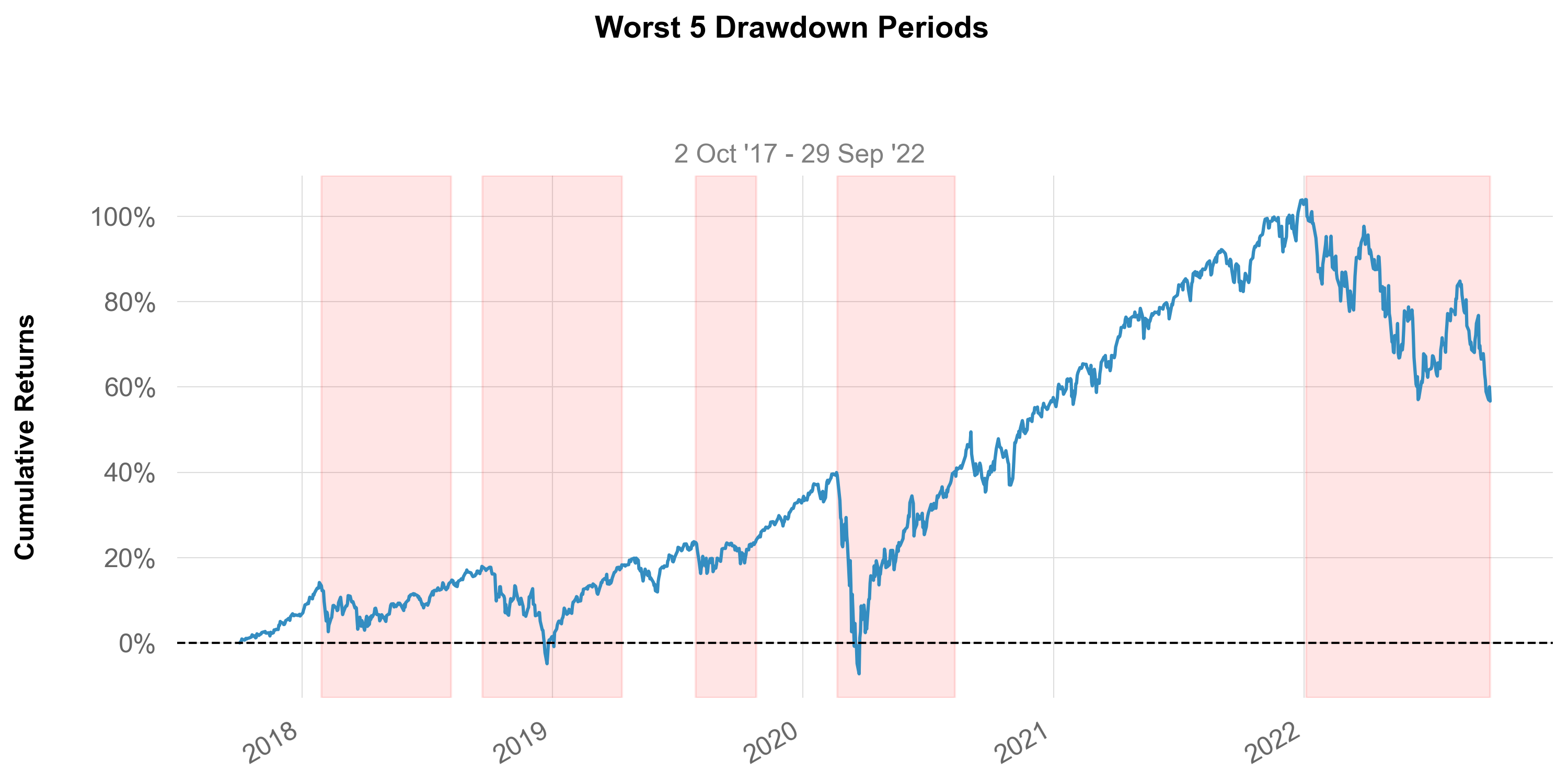

drawdowns_periods (returns, periods=5, lw=1.5, log_scale=False, fontname='Arial', grayscale=False, figsize=(10, 5), ylabel=True, subtitle=True, compounded=True, savefig=None, show=True, prepare_returns=True)

values = _utils.download_returns('SPY', '5y')

drawdowns_periods(values)

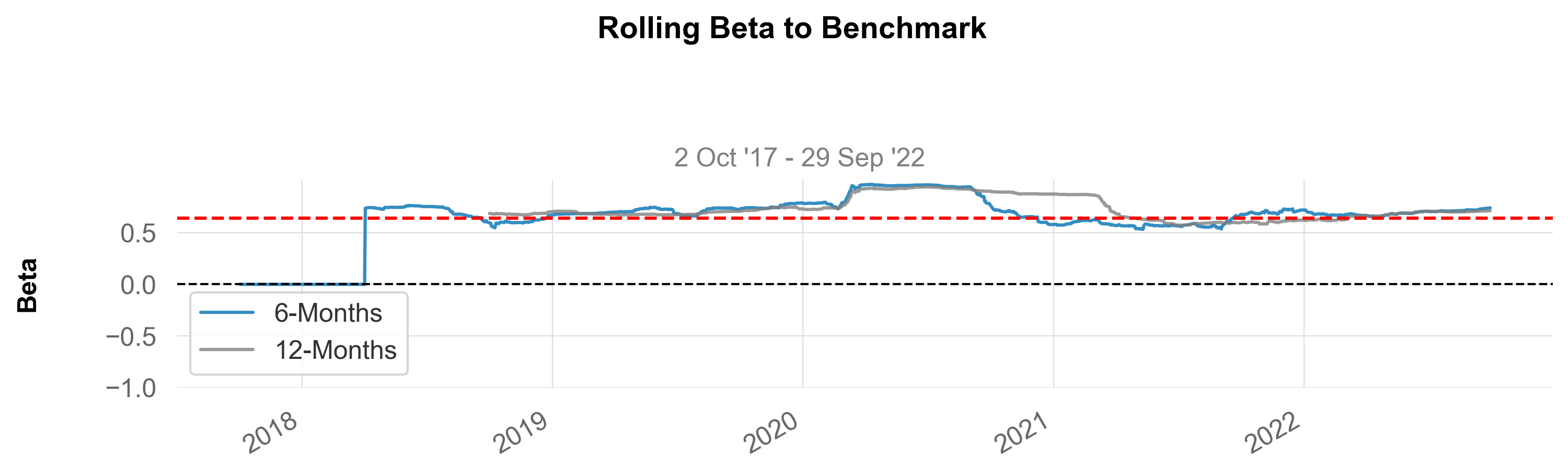

rolling_beta (returns, benchmark, benchmark_label='Benchmark', window1=126, window1_label='6-Months', window2=252, window2_label='12-Months', lw=1.5, fontname='Arial', grayscale=False, figsize=(10, 3), ylabel=True, subtitle=True, savefig=None, show=True, prepare_returns=True)

values = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

rolling_beta(values, benchmark)

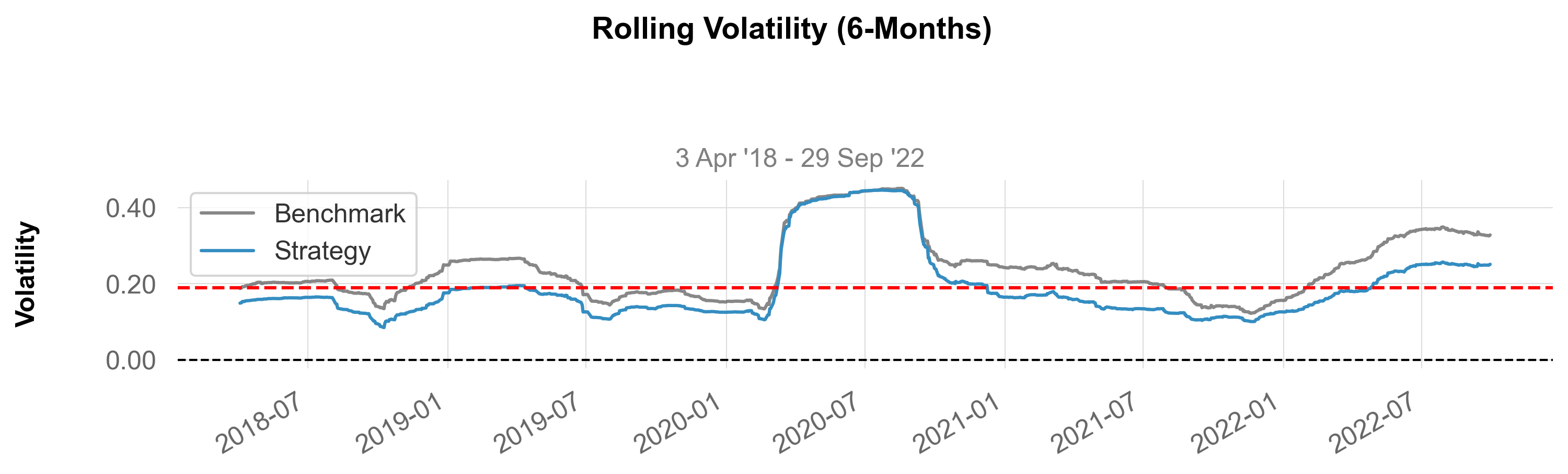

rolling_volatility (returns, benchmark=None, returns_label='Strategy', benchmark_label='Benchmark', period=126, period_label='6-Months', periods_per_year=252, lw=1.5, fontname='Arial', grayscale=False, figsize=(10, 3), ylabel='Volatility', subtitle=True, savefig=None, show=True)

values = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

rolling_volatility(values, benchmark)

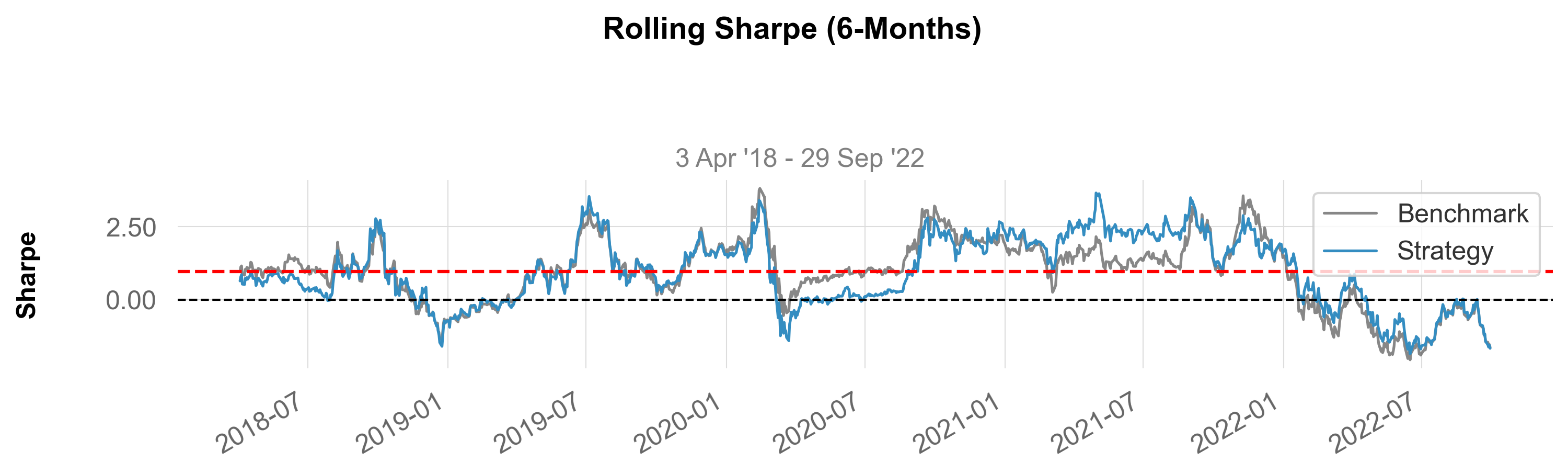

rolling_sharpe (returns, benchmark=None, rf=0.0, returns_label='Strategy', benchmark_label='Benchmark', period=126, period_label='6-Months', periods_per_year=252, lw=1.25, fontname='Arial', grayscale=False, figsize=(10, 3), ylabel='Sharpe', subtitle=True, savefig=None, show=True)

values = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

rolling_sharpe(values, benchmark)

rolling_sortino (returns, benchmark=None, rf=0.0, returns_label='Strategy', benchmark_label='Benchmark', period=126, period_label='6-Months', periods_per_year=252, lw=1.25, fontname='Arial', grayscale=False, figsize=(10, 3), ylabel='Sortino', subtitle=True, savefig=None, show=True)

values = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

rolling_sortino(values, benchmark)

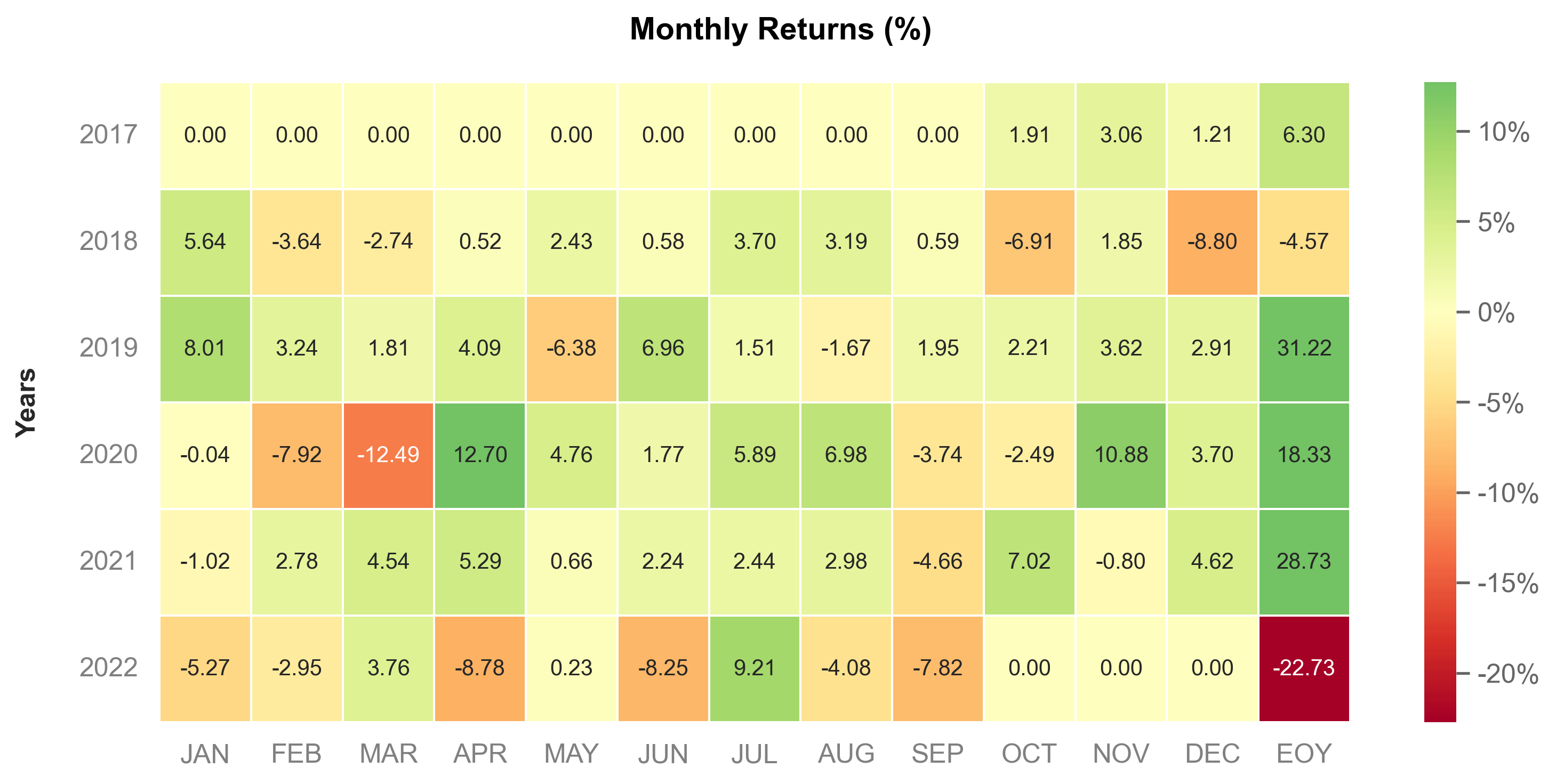

monthly_heatmap (returns, annot_size=10, figsize=(10, 5), cbar=True, square=False, compounded=True, eoy=False, grayscale=False, fontname='Arial', ylabel=True, savefig=None, show=True)

values = _utils.download_returns('SPY', '5y')

monthly_heatmap(values, eoy=True)

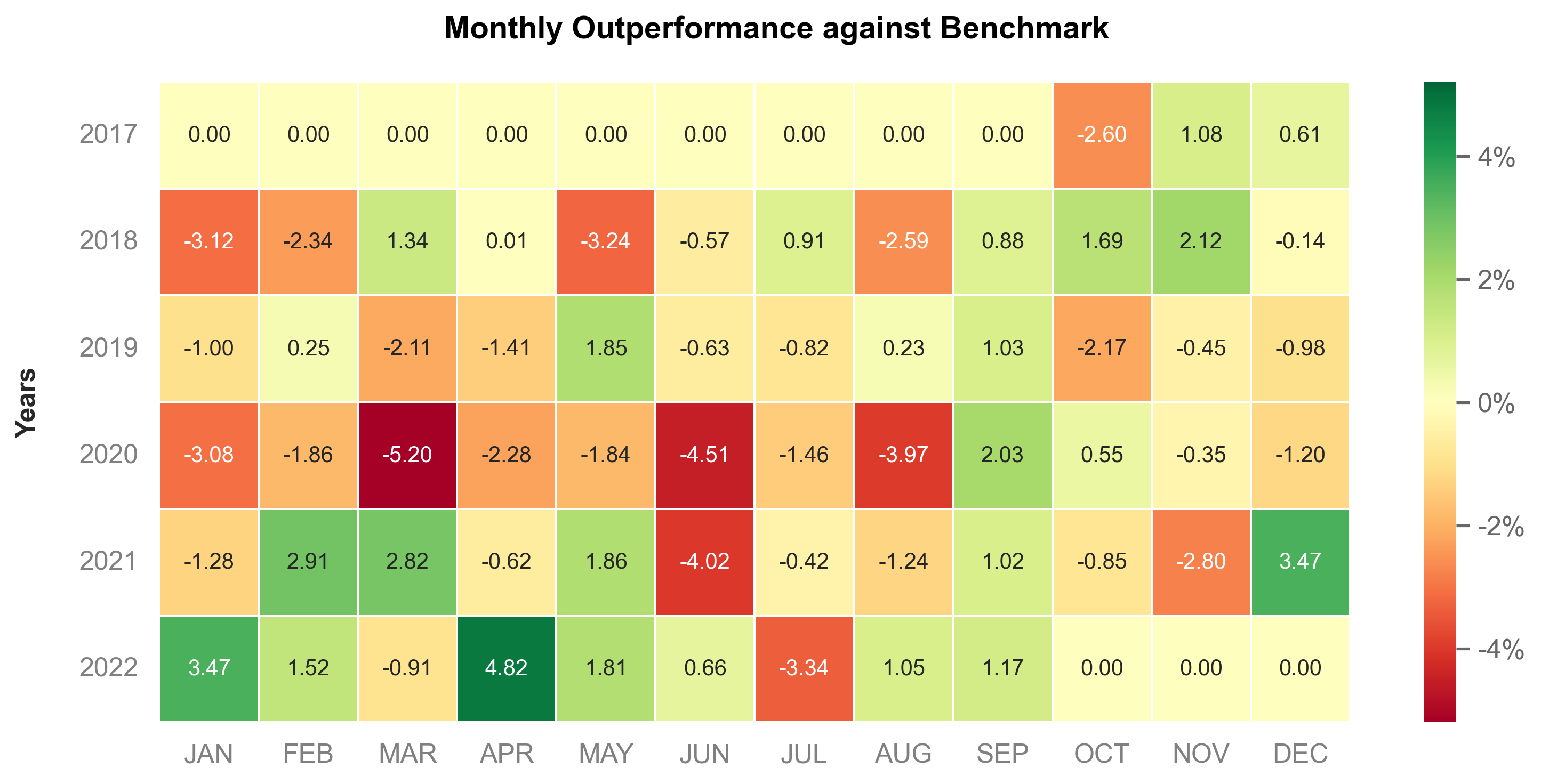

outperformance_heatmap (returns, benchmark=None, annot_size=10, figsize=(10, 5), cbar=True, square=False, benchmark_label='Benchmark', compounded=True, eoy=False, grayscale=False, fontname='Arial', ylabel=True, savefig=None, show=True)

values = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

outperformance_heatmap(values, benchmark)

monthly_returns (returns, annot_size=10, figsize=(10, 5), cbar=True, square=False, compounded=True, eoy=False, grayscale=False, fontname='Arial', ylabel=True, savefig=None, show=True)

A wrapper for monthly heatmaps