returns = pd.Series(np.array([0.03, 0.01, 0.05, -0.01, -0.03]))

compsum(returns)0 0.030000

1 0.040300

2 0.092315

3 0.081392

4 0.048950

dtype: float64compsum (returns)

Calculates cumulative compounded returns up to each day, for series of daily returns

returns = pd.Series(np.array([0.03, 0.01, 0.05, -0.01, -0.03]))

compsum(returns)0 0.030000

1 0.040300

2 0.092315

3 0.081392

4 0.048950

dtype: float64comp (returns)

Calculates total compounded return, for series of daily returns

returns = pd.Series(np.array([0.03, 0.01, 0.05, -0.01, -0.03]))

comp(returns)0.048950094500000096distribution (returns, compounded=True, prepare_returns=False)

Show the returns and outlier values based on IQR from a series of returns. Outliers are those more than 1.5 times the IQR from the Q1/Q3

expected_return (returns, aggregate=None, compounded=True, prepare_returns=True)

Returns the expected geometric return for a given period by calculating the geometric holding period return

The expected geometric return is: \[ \left(\prod\limits_{i=1}^{n}(p_{i})\right)^{(1/n)} -1\]

where \(p_{i}\) is 1+ the daily return: \(p_{i}=\frac{v_{i}}{v_{i-1}}=1+r_{i}\), where \(v_{i}\) and \(r_{i}\) are value and return of the asset on day \(i\) respectively

returns = pd.Series(np.array([0.03, 0.01, 0.05, -0.01, -0.03]))

expected_return(returns, aggregate=None, compounded=True,

prepare_returns=True)0.009603773872040255ghpr (retruns, aggregate=None, compounded=True)

Shorthand for expected_return()

geometric_mean (retruns, aggregate=None, compounded=True)

Shorthand for expected_return()

outliers (returns, quantile=0.95)

Returns series of outliers: all values greater than the quantile

returns = pd.Series(np.arange(1, 101, 1))

outliers(returns, quantile=.95)95 96

96 97

97 98

98 99

99 100

dtype: int32remove_outliers (returns, quantile=0.95)

Returns series of returns without the outliers on the top end

returns = pd.Series(np.arange(1, 101, 1))

remove_outliers(returns, quantile=.95).tail(10) # the range goes from [1,100] to [1,95]85 86

86 87

87 88

88 89

89 90

90 91

91 92

92 93

93 94

94 95

dtype: int32best (returns, aggregate=None, compounded=True, prepare_returns=False)

Returns the best day/month/week/quarter/year’s return

returns = _utils.download_returns('SPY', '5y')

best(returns)

#best(returns)0.09060315805687602worst (returns, aggregate=None, compounded=True, prepare_returns=False)

Returns the worst day/month/week/quarter/year’s return

returns = _utils.download_returns('SPY', '5y')

worst(returns)

#best(returns)-0.10942352331745997consecutive_wins (returns, aggregate=None, compounded=True, prepare_returns=False)

Returns the maximum consecutive wins by day/month/week/quarter/year

returns = _utils.download_returns('SPY', '5y')

consecutive_wins(returns)

#best(returns)11consecutive_losses (returns, aggregate=None, compounded=True, prepare_returns=False)

Returns the maximum consecutive losses by day/month/week/quarter/year

returns = _utils.download_returns('SPY', '5y')

consecutive_losses(returns)

#best(returns)8exposure (returns, prepare_returns=False)

Returns the market exposure time (returns != 0)

returns = _utils.download_returns('SPY', '5y')

exposure(returns)1.0win_rate (returns, aggregate=None, compounded=True, prepare_returns=False)

Calculates the win ratio for a period: (number of winning days)/(number of days in market)

returns = _utils.download_returns('SPY', '5y')

win_rate(returns)0.5542264752791068avg_return (returns, aggregate=None, compounded=True, prepare_returns=False)

Calculates the average return/trade return for a period

returns = _utils.download_returns('SPY', '5y')

avg_return(returns)0.0004451419089322777avg_win (returns, aggregate=None, compounded=True, prepare_returns=False)

Calculates the average winning return/trade return for a period

returns = _utils.download_returns('SPY', '5y')

avg_win(returns)0.008044224938256789avg_loss (returns, aggregate=None, compounded=True, prepare_returns=False)

Calculates the average low if return/trade return for a period

returns = _utils.download_returns('SPY', '5y')

avg_loss(returns)-0.009002736188760357volatility (returns, periods=252, annualize=True, prepare_returns=False)

Calculates the volatility of returns for a period

Calculate volatility as \(\text{vol.}=\sigma\sqrt{T}\) where \(\sigma\) is the standard deviations of returns and \(T\) the number of periods in the time horizon

returns = _utils.download_returns('SPY', '5y')

volatility(returns)0.20844063908238844rolling_volatility (returns, rolling_period=126, periods_per_year=252, prepare_returns=False)

Create time series of rolling volatility

returns = _utils.download_returns('SPY', '1y')

rolling_volatility(returns).tail(10)Date

2022-09-16 0.248680

2022-09-19 0.248414

2022-09-20 0.248865

2022-09-21 0.249286

2022-09-22 0.248944

2022-09-23 0.248828

2022-09-26 0.248951

2022-09-27 0.248649

2022-09-28 0.249690

2022-09-29 0.251102

Name: Close, dtype: float64implied_volatility (returns, periods=252, annualize=False)

Calculates the implied volatility of returns for a period

Implied volatility is defined here as the standard deviation of the log returns. This works under the assumption that returns are lognormally distributed and so the log of returns is a normal distribution.

returns = _utils.download_returns('SPY', '1y')

implied_volatility(returns)0.013801893088772903autocorr_penalty (returns, prepare_returns=False)

Metric to account for auto correlation

returns = _utils.download_returns('SPY', '5y')

autocorr_penalty(returns)1.1893156409496177smart_sharpe (returns, rf=0.0, periods=252, annualize=True)

Sharpe ratio, penalised with autocorrelation penalty

returns = _utils.download_returns('SPY', '5y')

smart_sharpe(returns)0.4510622023704182rolling_sharpe (returns, rf=0.0, rolling_period=126, annualize=True, periods_per_year=252, prepare_returns=False)

Calculate rolling Sharpe ratio over a period

returns = _utils.download_returns('SPY', '5y')

rolling_sharpe(returns).tail(10)Date

2022-09-16 -0.864632

2022-09-19 -0.891301

2022-09-20 -0.979586

2022-09-21 -1.211758

2022-09-22 -1.177445

2022-09-23 -1.433826

2022-09-26 -1.551825

2022-09-27 -1.631454

2022-09-28 -1.566138

2022-09-29 -1.674526

Name: Close, dtype: float64sortino (returns, rf=0, periods=252, annualize=True, smart=False, prepare_returns=False)

Calculates the sortino ratio of access returns If rf is non-zero, you must specify periods. In this case, rf is assumed to be expressed in yearly (annualized) terms Calculation is based on this paper by Red Rock Capital http://www.redrockcapital.com/Sortino__A__Sharper__Ratio_Red_Rock_Capital.pdf

Calculates Sortino ratio as \(\frac{\text{Expected Excess Return}}{\text{Downside Deviation}}\) where for \(n\) periods the Downside deviation is \(\sqrt{\frac{\sum d^{2}}{n}}\) where \(d\) is an excess return less than 0, and the expected excess return is the mean excess return, and annualised

returns = _utils.download_returns('SPY', '5y')

sortino(returns)0.7310777239511432smart_sortino (returns, rf=0, periods=252, annualize=True)

Calculates Smart Sortino ratio, adding an autocorrelation penalty

returns = _utils.download_returns('SPY', '5y')

smart_sortino(returns)0.6147043287347095def adjusted_sortino(returns, rf=0, periods=252, annualize=True, smart=False):

"""

Jack Schwager's version of the Sortino ratio allows for

direct comparisons to the Sharpe. See here for more info:

https://archive.is/wip/2rwFW

"""

data = sortino(

returns, rf, periods=periods, annualize=annualize, smart=smart)

return data / sqrt(2)The adjusted sortino is defined as \(\text{Adj. Sortino}=\text{Sortino}/\sqrt{2}\)

returns = _utils.download_returns('SPY', '5y')

adjusted_sortino(returns)0.5169498730432484rolling_sortino (returns, rf=0, rolling_period=126, annualize=True, periods_per_year=252, **kwargs)

returns = _utils.download_returns('SPY', '5y')

rolling_sortino(returns).tail(10)Date

2022-09-16 -1.119173

2022-09-19 -1.152463

2022-09-20 -1.264410

2022-09-21 -1.554069

2022-09-22 -1.511805

2022-09-23 -1.826545

2022-09-26 -1.972788

2022-09-27 -2.071153

2022-09-28 -1.996554

2022-09-29 -2.124861

Name: Close, dtype: float64skew (returns, prepare_returns=False)

Calculates returns’ skewness (the degree of asymmetry of a distribution around its mean)

The skew is defined as \(\text{Skew}(X)=\frac{E[(X-\mu)^{3}]}{E[(X-\mu)^{2}]^{3/2}}=\frac{\mu_{3}}{\sigma^{3}}\), where \(\mu\) is mean, \(\sigma\) stadard deviation and \(\mu_{3}\), third moment of inertia.

returns = _utils.download_returns('SPY', '5y')

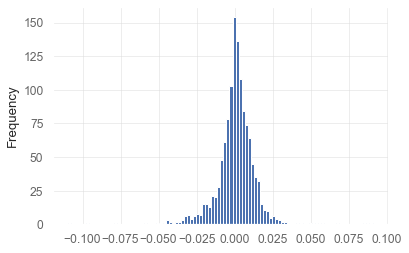

skew(returns)-0.6567130752131589kurtosis (returns, prepare_returns=False)

Calculates returns’ kurtosis (the degree to which a distribution peak compared to a normal distribution)

The kurtosis is defined as \(\text{Kurt}(X)=\frac{E[(X-\mu)^{4}]}{E[(X-\mu)^{2}]^{2}}=\frac{\mu_{4}}{\sigma^{2}}\), where \(\mu\) is mean, \(\sigma\) stadard deviation and \(\mu_{4}\), fourth moment of inertia. A measure of ‘tailed’: higher kurtosis means fatter tails.

returns = _utils.download_returns('SPY', '5y')

kurtosis(returns)11.996182480024226<AxesSubplot:ylabel='Frequency'>

probabilistic_ratio (series, rf=0.0, base='sharpe', periods=252, annualize=False, smart=False)

probabilistic_sharpe_ratio (series, rf=0.0, periods=252, annualize=False, smart=False)

The probabilistic Sharpe Ratio

returns = _utils.download_returns('SPY', '5y')

probabilistic_sharpe_ratio(returns)0.8816407449051655probabilistic_sortino_ratio (series, rf=0.0, periods=252, annualize=False, smart=False)

The probabilistic Sortino Ratio

returns = _utils.download_returns('SPY', '5y')

probabilistic_sortino_ratio(returns)0.9456555568118186probabilistic_adjusted_sortino_ratio (series, rf=0.0, periods=252, annualize=False, smart=False)

The probabilistic adj. Sortino Ratio

returns = _utils.download_returns('SPY', '5y')

probabilistic_adjusted_sortino_ratio(returns)0.8730193107071486omega (returns, rf=0.0, required_return=0.0, periods=252, **kwargs)

Determines the Omega ratio of a strategy. See https://en.wikipedia.org/wiki/Omega_ratio for more details.

This is broken

returns = _utils.download_returns('SPY', '5y')

#omega(returns, 0.01)gain_to_pain_ratio (returns, rf=0, resolution='D', **kwargs)

Jack Schwager’s GPR. See here for more info: https://archive.is/wip/2rwFW

This seems to be wrong

returns = _utils.download_returns('SPY', '5y')

gain_to_pain_ratio(returns, 10)0.11091999229680034cagr (returns, rf=0.0, compounded=True, **kwargs)

Calculates the communicative annualized growth return (CAGR%) of access returns If rf is non-zero, you must specify periods?. In this case, rf is assumed to be expressed in yearly (annualized) terms

Check

returns = _utils.download_returns('SPY', '5y')

cagr(returns, 10)0.09407550605477089rar (returns, rf=0.0, **kwargs)

Calculates the risk-adjusted return of access returns (CAGR / exposure. takes time into account.) If rf is non-zero, you must specify periods. In this case, rf is assumed to be expressed in yearly (annualized) terms

Check if this should be excess return

returns = _utils.download_returns('SPY', '5y')

rar(returns)0.09407549161897544max_drawdown (returns)

Calculates the maximum drawdown

returns = _utils.download_returns('SPY', '5y')

max_drawdown(returns)-0.3371726193896011to_drawdown_series (returns)

Convert returns series to drawdown series

returns = _utils.download_returns('SPY', '5y')

to_drawdown_series(returns).tail(10)Date

2022-09-16 -0.183555

2022-09-19 -0.177223

2022-09-20 -0.186668

2022-09-21 -0.200855

2022-09-22 -0.207568

2022-09-23 -0.220845

2022-09-26 -0.228553

2022-09-27 -0.230522

2022-09-28 -0.215382

2022-09-29 -0.231771

Name: Close, dtype: float64calmar (returns, prepare_returns=False)

Calculates the calmar ratio (CAGR% / MaxDD%)

returns = _utils.download_returns('SPY', '5y')

calmar(returns)0.27901279782780064ulcer_index (returns)

Calculates the ulcer index score (downside risk measurment)

Define properly

returns = _utils.download_returns('SPY', '5y')

ulcer_index(returns)0.07637641267955013ulcer_performance_index (returns, rf=0)

Calculates the ulcer index score (downside risk measurment)

returns = _utils.download_returns('SPY', '5y')

ulcer_performance_index(returns)7.4215621009669315upi (returns, rf=0)

Shorthand for ulcer_performance_index()

risk_of_ruin (returns, prepare_returns=False)

Calculates the risk of ruin (the likelihood of losing all one’s investment capital)

Check definition

returns = _utils.download_returns('SPY', '5y')

risk_of_ruin(returns)0.0ror (returns)

Shorthand for risk_of_ruin()

value_at_risk (returns, sigma=1, confidence=0.95, prepare_returns=False)

Calculats the daily value-at-risk (variance-covariance calculation with confidence n)

Define

returns = _utils.download_returns('SPY', '5y')

value_at_risk(returns)-0.021154066958981442var (returns, sigma=1, confidence=0.95, prepare_returns=False)

Shorthand for value_at_risk()

conditional_value_at_risk (returns, sigma=1, confidence=0.95, prepare_returns=False)

Calculats the conditional daily value-at-risk (aka expected shortfall) quantifies the amount of tail risk an investment

returns = _utils.download_returns('SPY', '5y')

conditional_value_at_risk(returns)-0.03378474064120063cvar (returns, sigma=1, confidence=0.95, prepare_returns=False)

Shorthand for conditional_value_at_risk()

expected_shortfall (returns, sigma=1, confidence=0.95, prepare_returns=False)

Shorthand for conditional_value_at_risk()

serenity_index (returns, rf=0)

Calculates the serenity index score (https://www.keyquant.com/Download/GetFile?Filename=%5CPublications%5CKeyQuant_WhitePaper_APT_Part1.pdf)

returns = _utils.download_returns('SPY', '5y')

serenity_index(returns)0.5104927720686929tail_ratio (returns, cutoff=0.95, prepare_returns=False)

Measures the ratio between the right (95%) and left tail (5%).

returns = _utils.download_returns('SPY', '5y')

tail_ratio(returns)0.8246500295451326payoff_ratio (returns, prepare_returns=False)

Measures the payoff ratio (average win/average loss)

Should probably rate this by win rate/loss rate

returns = _utils.download_returns('SPY', '5y')

payoff_ratio(returns)0.8935312962081646win_loss_ratio (returns, prepare_returns=False)

Shorthand for payoff_ratio()

profit_ratio (returns, prepare_returns=False)

Measures the profit ratio (win ratio / loss ratio)

returns = _utils.download_returns('SPY', '5y')

profit_ratio(returns)0.7104803267194572profit_factor (returns, prepare_returns=False)

Measures the profit ratio (wins/loss)

returns = _utils.download_returns('SPY', '5y')

profit_factor(returns)1.1109199478795606cpc_index (returns, prepare_returns=False)

Measures the cpc ratio (profit factor * win % * win loss ratio)

returns = _utils.download_returns('SPY', '5y')

profit_factor(returns)1.1109200029518147common_sense_ratio (returns, prepare_returns=False)

Measures the common sense ratio (profit factor * tail ratio)

returns = _utils.download_returns('SPY', '5y')

common_sense_ratio(returns)0.9161143659778377outlier_win_ratio (returns, quantile=0.99, prepare_returns=False)

Calculates the outlier winners ratio 99th percentile of returns / mean positive return

returns = _utils.download_returns('SPY', '5y')

outlier_win_ratio(returns)3.8800605330519113outlier_loss_ratio (returns, quantile=0.01, prepare_returns=False)

Calculates the outlier losers ratio 1st percentile of returns / mean negative return

returns = _utils.download_returns('SPY', '5y')

outlier_loss_ratio(returns)4.188328392594448recovery_factor (returns, prepare_returns=False)

Measures how fast the strategy recovers from drawdowns

returns = _utils.download_returns('SPY', '5y')

recovery_factor(returns)1.6811327076863491risk_return_ratio (returns, prepare_returns=True)

Calculates the return / risk ratio (sharpe ratio without factoring in the risk-free rate)

returns = _utils.download_returns('SPY', '5y')

risk_return_ratio(returns)0.033793529561903915drawdown_details (drawdown)

Calculates drawdown details, including start/end/valley dates, duration, max drawdown and max dd for 99% of the dd period for every drawdown period

returns = _utils.download_returns('SPY', '5y')

drawdown = to_drawdown_series(returns)

drawdown_details(drawdown).tail(10)| start | valley | end | days | max drawdown | 99% max drawdown | |

|---|---|---|---|---|---|---|

| 86 | 2021-09-03 | 2021-10-04 | 2021-10-20 | 47 | -5.114137 | -5.003459 |

| 87 | 2021-10-22 | 2021-10-22 | 2021-10-25 | 3 | -0.103615 | 0.000000 |

| 88 | 2021-10-27 | 2021-10-27 | 2021-10-28 | 1 | -0.443010 | 0.000000 |

| 89 | 2021-11-09 | 2021-11-10 | 2021-11-16 | 7 | -1.132363 | -1.100381 |

| 90 | 2021-11-17 | 2021-11-17 | 2021-11-18 | 1 | -0.242927 | 0.000000 |

| 91 | 2021-11-19 | 2021-12-01 | 2021-12-10 | 21 | -4.093850 | -3.472205 |

| 92 | 2021-12-13 | 2021-12-20 | 2021-12-23 | 10 | -3.008357 | -1.965921 |

| 93 | 2021-12-28 | 2021-12-28 | 2021-12-29 | 1 | -0.081728 | 0.000000 |

| 94 | 2021-12-30 | 2021-12-31 | 2022-01-03 | 4 | -0.527776 | -0.276447 |

| 95 | 2022-01-04 | 2022-09-29 | 2022-09-29 | 268 | -23.177148 | -23.009976 |

kelly_criterion (returns, prepare_returns=False)

Calculates the recommended maximum amount of capital that should be allocated to the given strategy, based on the Kelly Criterion (http://en.wikipedia.org/wiki/Kelly_criterion)

returns = _utils.download_returns('SPY', '5y')

kelly_criterion(returns)0.05533682629177291r_squared (returns, benchmark, prepare_returns=True)

Measures the straight line fit of the equity curve

SPY = _utils.download_prices('SPY', '5y')

r_squared(SPY, 'QQQ')0.8657597594693889r2 (returns, benchmark)

Shorthand for r_squared()

information_ratio (returns, benchmark, prepare_returns=True)

Calculates the information ratio (basically the risk return ratio of the net profits)

SPY = _utils.download_prices('SPY', '5y')

information_ratio(SPY, 'QQQ')-0.034145732893584566greeks (returns, benchmark, periods=252.0, prepare_returns=True)

Calculates alpha and beta of the portfolio

SPY = _utils.download_prices('SPY', '5y')

greeks(SPY, 'QQQ')beta 0.766525

alpha -0.014009

dtype: float64rolling_greeks (returns, benchmark, periods=252, prepare_returns=True)

Calculates rolling alpha and beta of the portfolio

SPY = _utils.download_prices('SPY', '5y')

rolling_greeks(SPY, 'QQQ').tail(10)| beta | alpha | |

|---|---|---|

| Date | ||

| 2022-09-16 | 0.711193 | -0.000020 |

| 2022-09-19 | 0.711200 | -0.000020 |

| 2022-09-20 | 0.711199 | -0.000020 |

| 2022-09-21 | 0.712228 | -0.000020 |

| 2022-09-22 | 0.711855 | -0.000020 |

| 2022-09-23 | 0.712161 | -0.000020 |

| 2022-09-26 | 0.712399 | -0.000020 |

| 2022-09-27 | 0.712574 | -0.000020 |

| 2022-09-28 | 0.713869 | -0.000021 |

| 2022-09-29 | 0.714026 | -0.000021 |

treynor_ratio (returns, benchmark, periods=252.0, rf=0.0, prepare_returns=True)

Calculates the Treynor ratio Args: * returns (Series, DataFrame): Input return series * benchmatk (String, Series, DataFrame): Benchmark to compare beta to * periods (int): Freq. of returns (252/365 for daily, 12 for monthly)

SPY = _utils.download_prices('SPY', '5y')

treynor_ratio(SPY, 'QQQ')0.7394830437816903compare (returns, benchmark, aggregate=None, compounded=True, round_vals=None, prepare_returns=True)

Compare returns to benchmark on a day/week/month/quarter/year basis

SPY = _utils.download_returns('SPY', '5y')

compare(SPY, 'QQQ', aggregate = 'M').tail(12)| Returns | Benchmark | Multiplier | Won | |

|---|---|---|---|---|

| (2021, 10) | 7.016350 | 7.864013 | 0.892210 | - |

| (2021, 11) | -0.803480 | 1.996842 | -0.402376 | - |

| (2021, 12) | 4.624778 | 1.152342 | 4.013372 | + |

| (2022, 1) | -5.274126 | -8.747021 | 0.602963 | + |

| (2022, 2) | -2.951699 | -4.475968 | 0.659455 | + |

| (2022, 3) | 3.759043 | 4.667878 | 0.805300 | - |

| (2022, 4) | -8.776911 | -13.595739 | 0.645563 | + |

| (2022, 5) | 0.225728 | -1.586593 | -0.142272 | + |

| (2022, 6) | -8.246043 | -8.907885 | 0.925702 | + |

| (2022, 7) | 9.208745 | 12.551730 | 0.733663 | - |

| (2022, 8) | -4.080199 | -5.132186 | 0.795022 | + |

| (2022, 9) | -7.819145 | -8.992359 | 0.869532 | + |

Note that these returns are already formatted in percentage terms

monthly_returns (returns, eoy=True, compounded=True, prepare_returns=True)

Calculates monthly returns

SPY = _utils.download_prices('SPY', '5Y')

monthly_returns(SPY)| JAN | FEB | MAR | APR | MAY | JUN | JUL | AUG | SEP | OCT | NOV | DEC | EOY | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 2017 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.000000 | 0.019142 | 0.030566 | 0.012128 | 0.063031 |

| 2018 | 0.056359 | -0.036360 | -0.027411 | 0.005168 | 0.024309 | 0.005751 | 0.037047 | 0.031920 | 0.005945 | -0.069104 | 0.018549 | -0.088049 | -0.045690 |

| 2019 | 0.080066 | 0.032416 | 0.018100 | 0.040852 | -0.063771 | 0.069586 | 0.015119 | -0.016743 | 0.019458 | 0.022105 | 0.036198 | 0.029055 | 0.312239 |

| 2020 | -0.000404 | -0.079166 | -0.124871 | 0.126983 | 0.047645 | 0.017735 | 0.058892 | 0.069797 | -0.037444 | -0.024933 | 0.108777 | 0.037049 | 0.183316 |

| 2021 | -0.010191 | 0.027805 | 0.045399 | 0.052911 | 0.006566 | 0.022427 | 0.024413 | 0.029760 | -0.046605 | 0.070163 | -0.008035 | 0.046248 | 0.287287 |

| 2022 | -0.052741 | -0.029517 | 0.037590 | -0.087769 | 0.002257 | -0.082460 | 0.092087 | -0.040802 | -0.078191 | 0.000000 | 0.000000 | 0.000000 | -0.227324 |