source

metrics

metrics (returns, benchmark=None, rf=0.0, display=True, mode='basic',

sep=False, compounded=True, periods_per_year=252,

prepare_returns=True, match_dates=False, **kwargs)

returns = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

# √ may be encodable

metrics(returns, benchmark, returns_title = 'SPY', benchmark_title = 'QQQ')

SPY QQQ

------------------ ---------- ----------

Start Period 2017-10-02 2017-10-02

End Period 2022-09-30 2022-09-30

Risk-Free Rate 0.0% 0.0%

Time in Market 100.0% 100.0%

Cumulative Return 56.11% 92.81%

CAGR 9.32% 14.04%

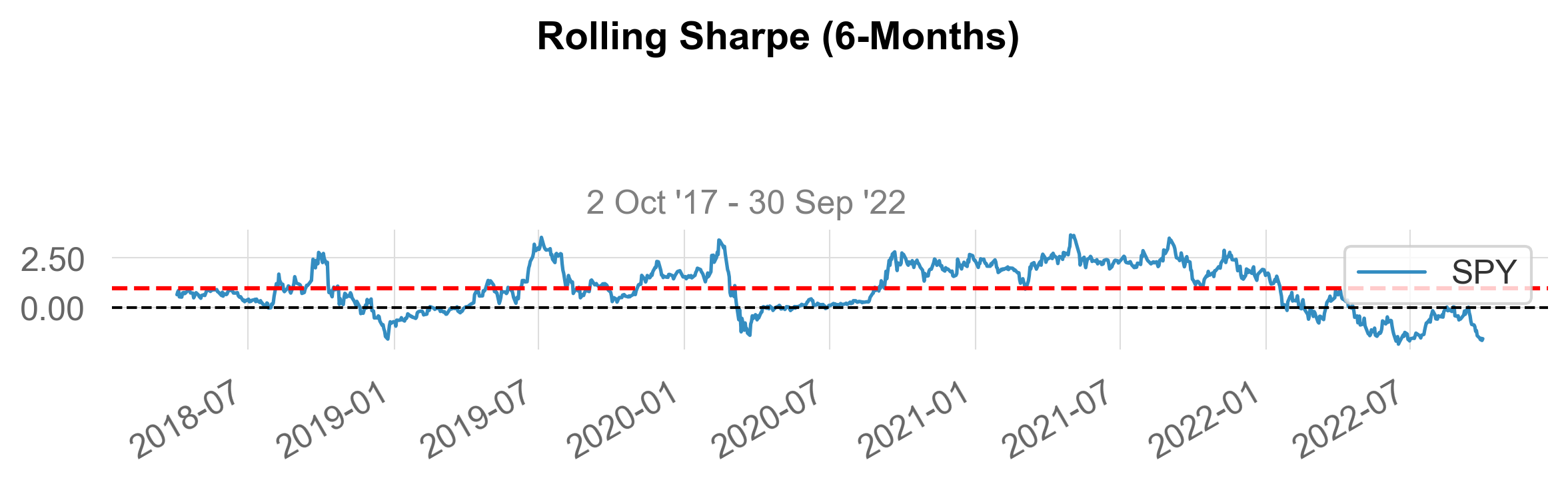

Sharpe 0.53 0.65

Prob. Sharpe Ratio 88.01% 92.36%

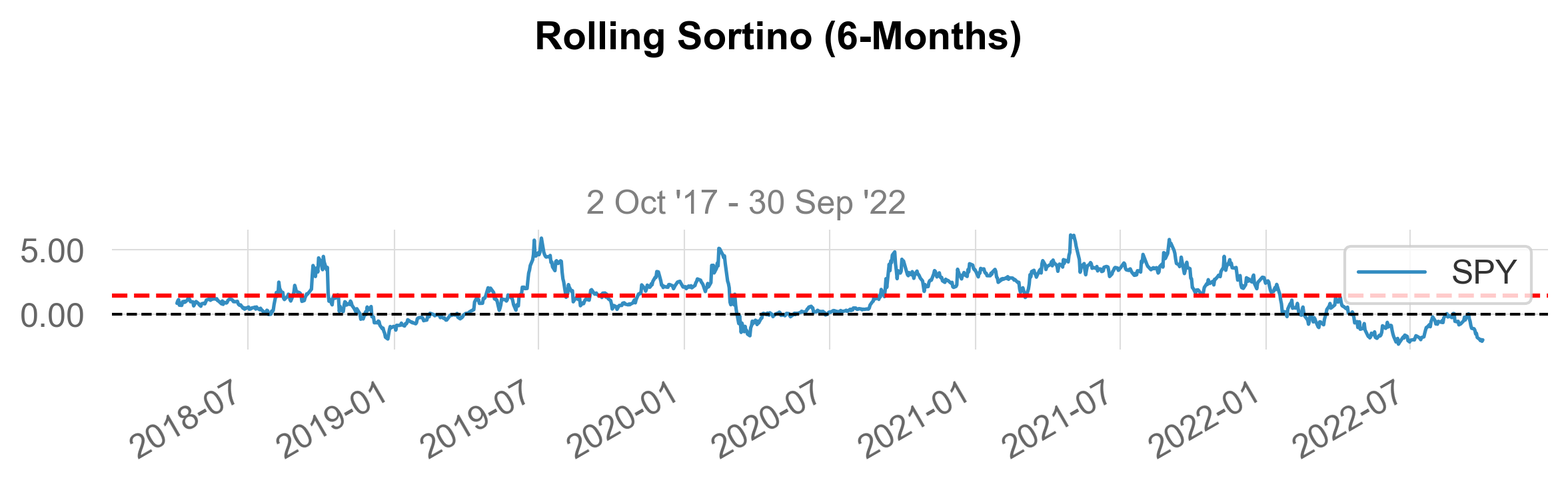

Sortino 0.73 0.89

Sortino/$\sqrt{2}$ 0.51 0.63

Omega 1.11 1.11

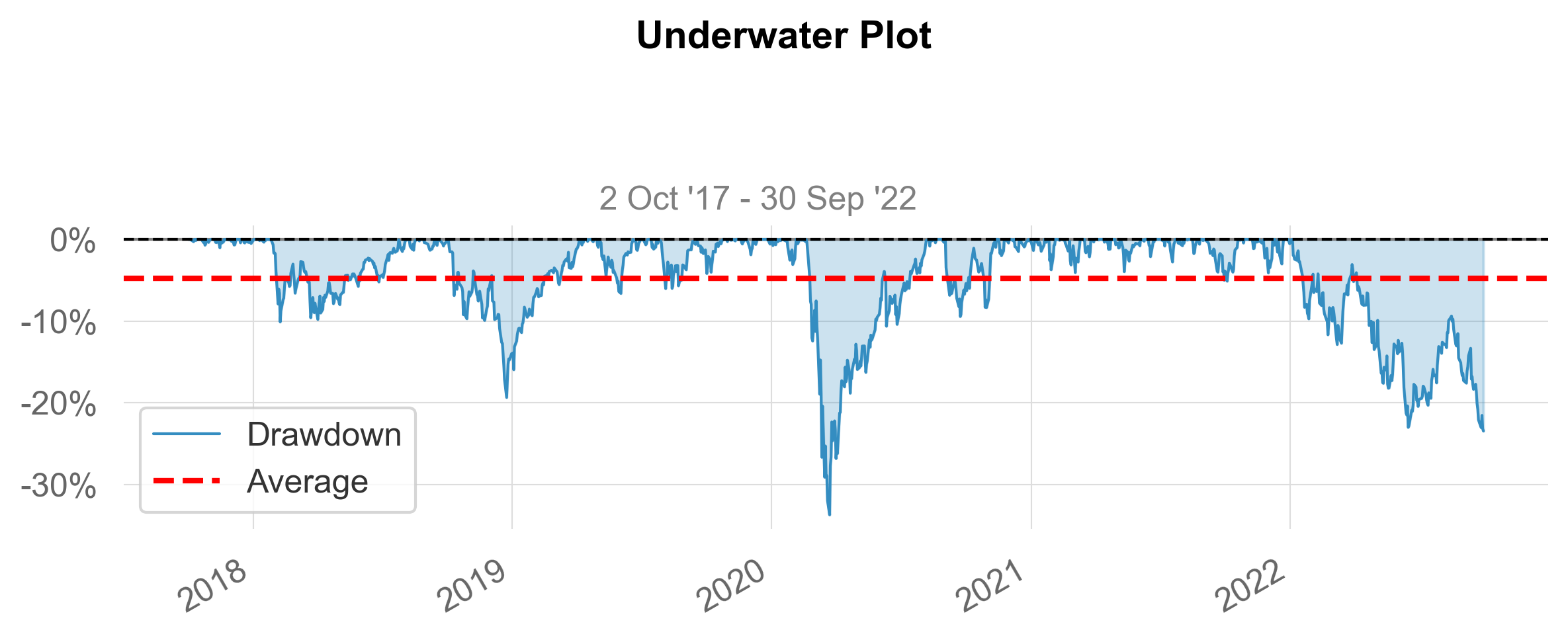

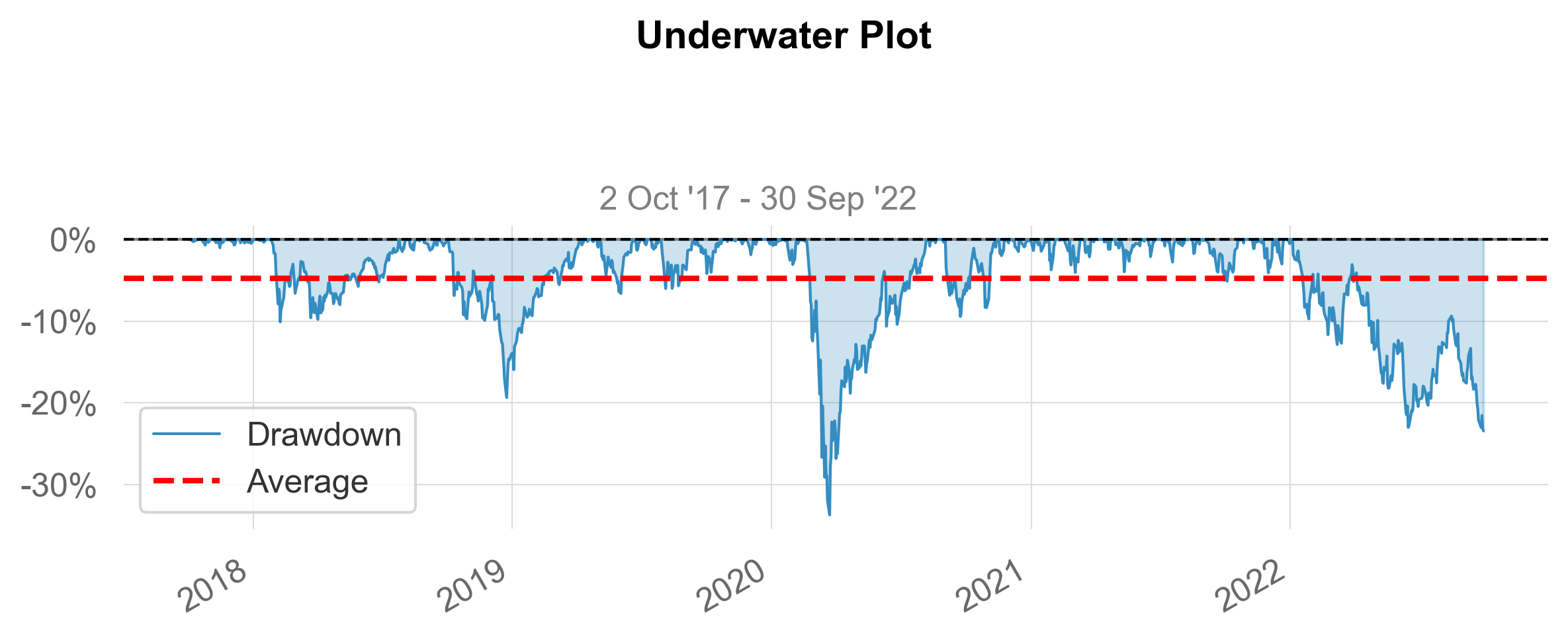

Max Drawdown -33.72% -32.65%

Longest DD Days 269 276

Gain/Pain Ratio 0.11 0.13

Gain/Pain (1M) 0.57 0.75

Payoff Ratio 0.85 0.85

Profit Factor 1.11 1.13

Common Sense Ratio 0.92 0.97

CPC Index 0.52 0.54

Tail Ratio 0.83 0.86

Outlier Win Ratio 4.46 3.47

Outlier Loss Ratio 4.57 3.45

MTD -8.16% -9.19%

3M -4.57% -4.24%

6M -21.02% -26.65%

YTD -23.02% -31.48%

1Y -15.54% -24.02%

3Y (ann.) 7.97% 12.44%

5Y (ann.) 9.0% 13.39%

10Y (ann.) 9.32% 14.04%

All-time (ann.) 9.32% 14.04%

Avg. Drawdown -1.92% -3.07%

Avg. Drawdown Days 16 19

Recovery Factor 1.66 2.84

Ulcer Index 0.08 0.1

Serenity Index 0.66 0.78

source

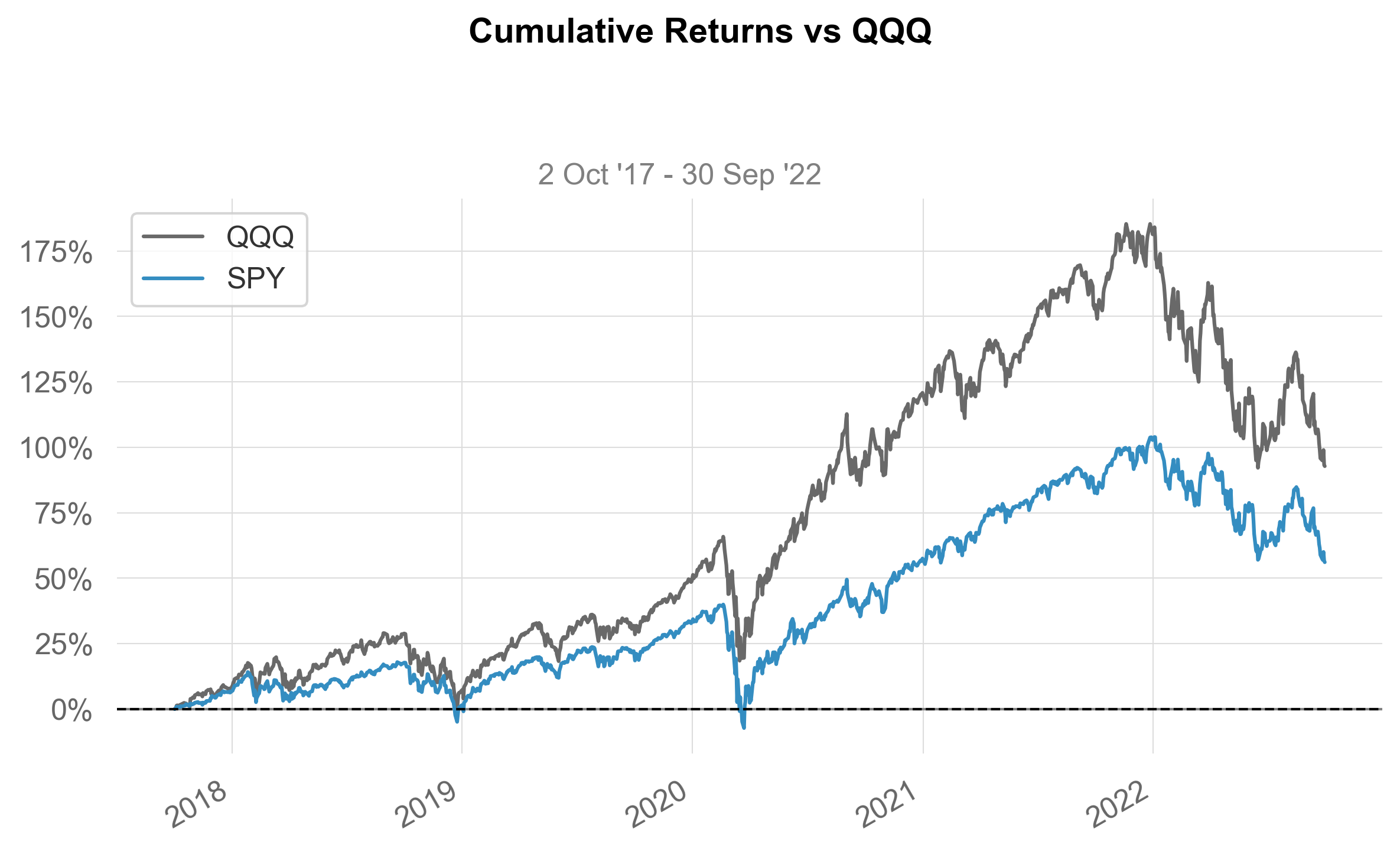

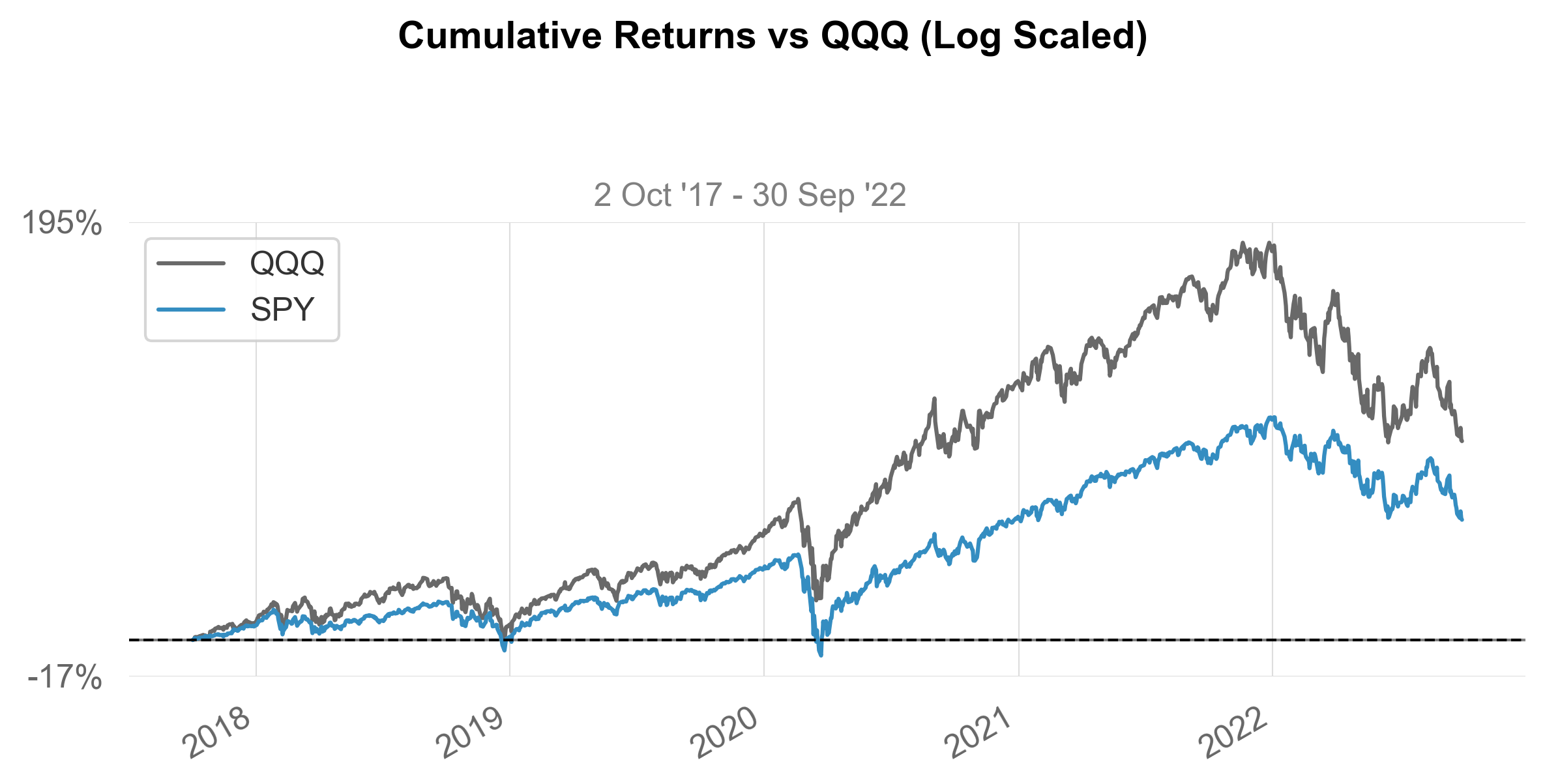

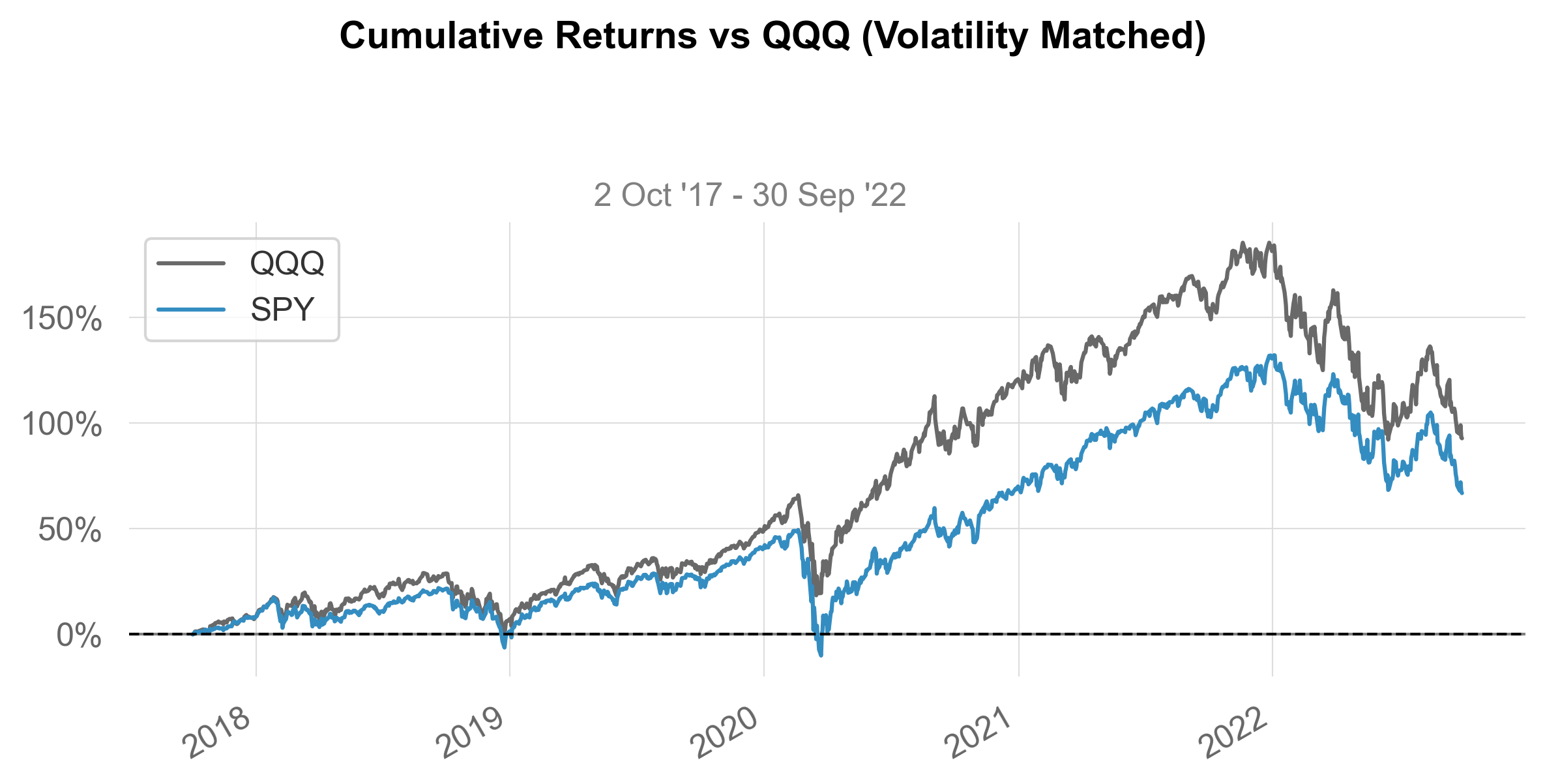

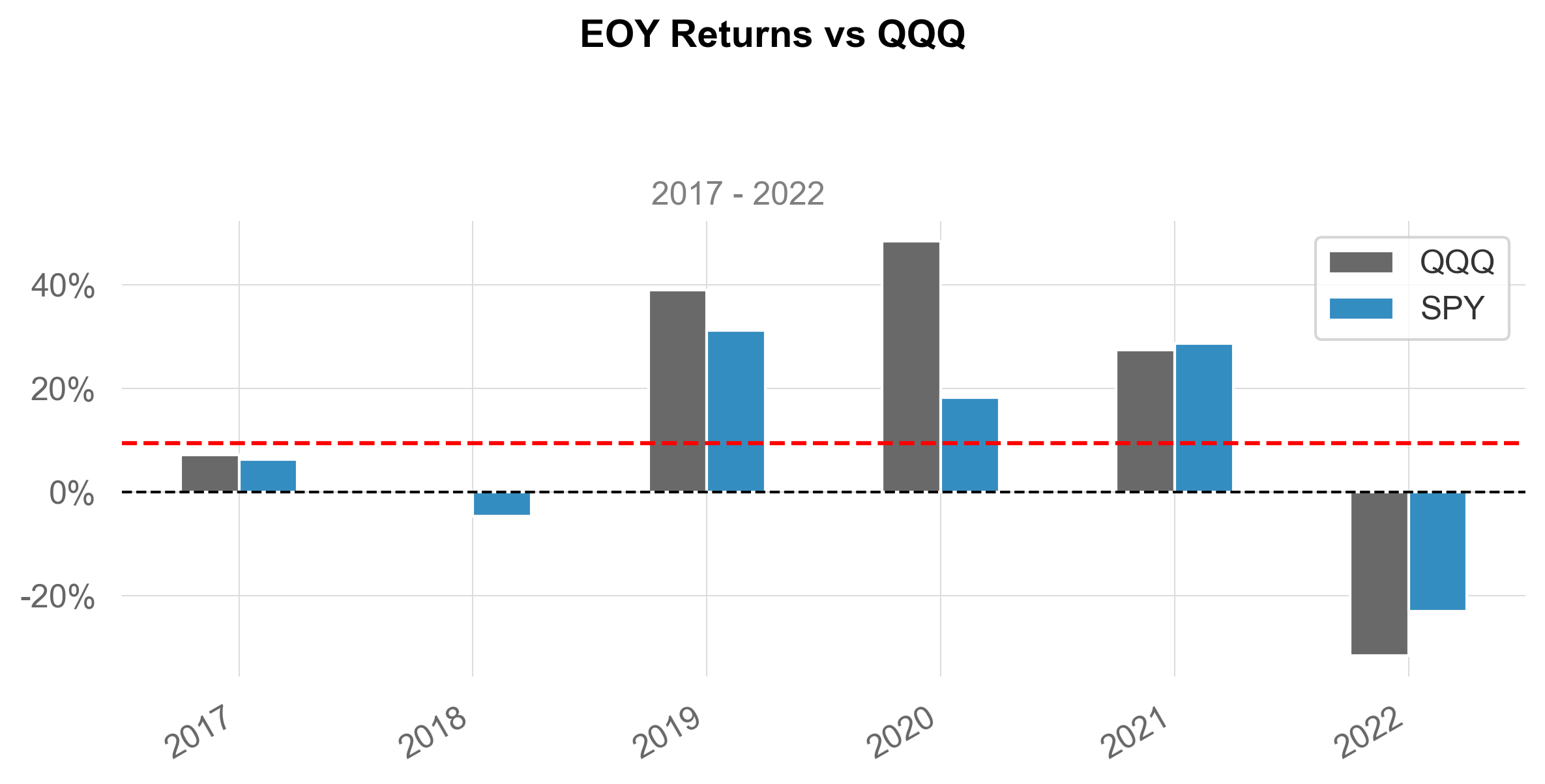

plots

plots (returns, benchmark=None, grayscale=False, figsize=(8, 5),

mode='basic', compounded=True, periods_per_year=252,

prepare_returns=True, match_dates=False, **kwargs)

returns = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

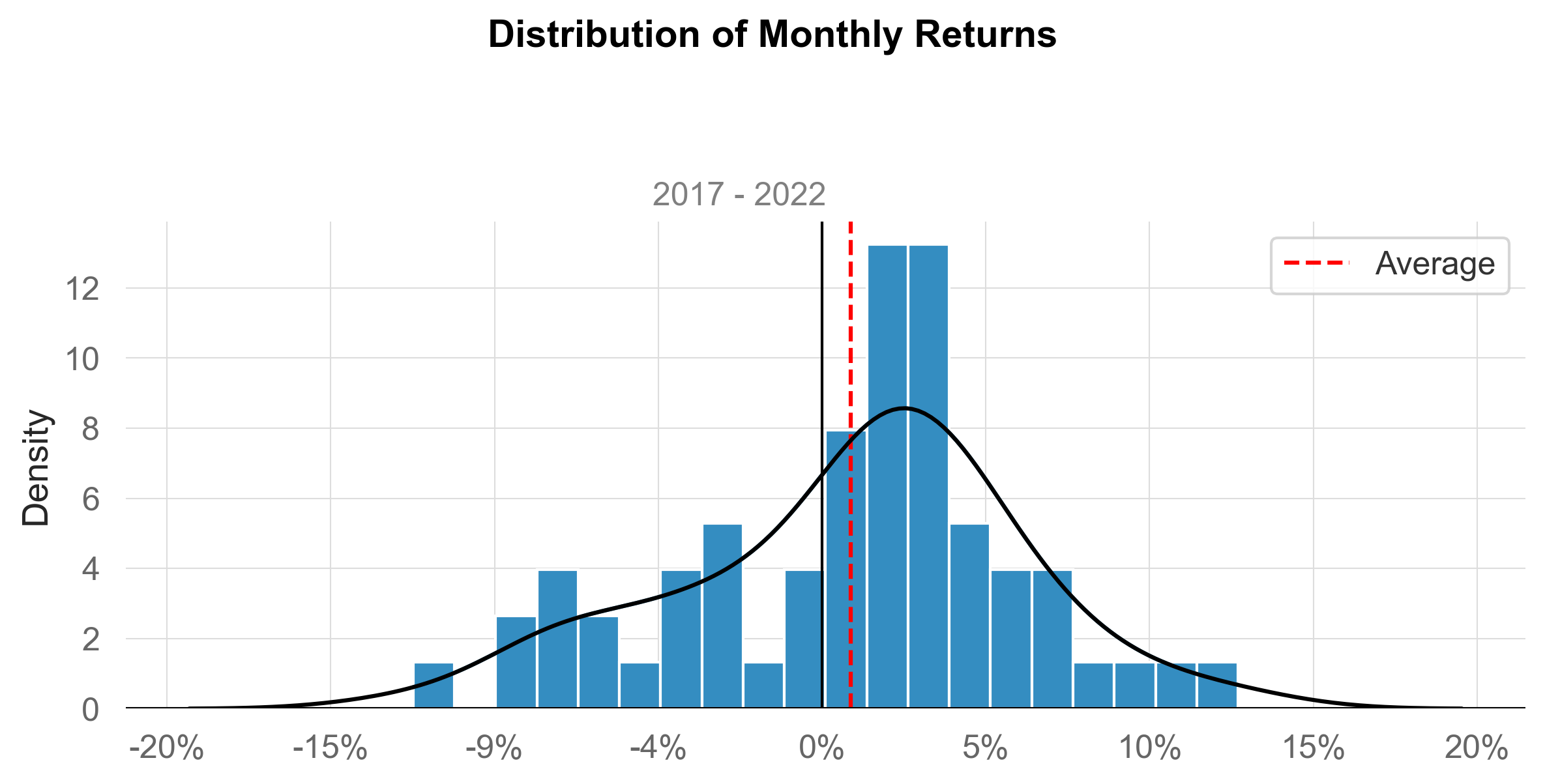

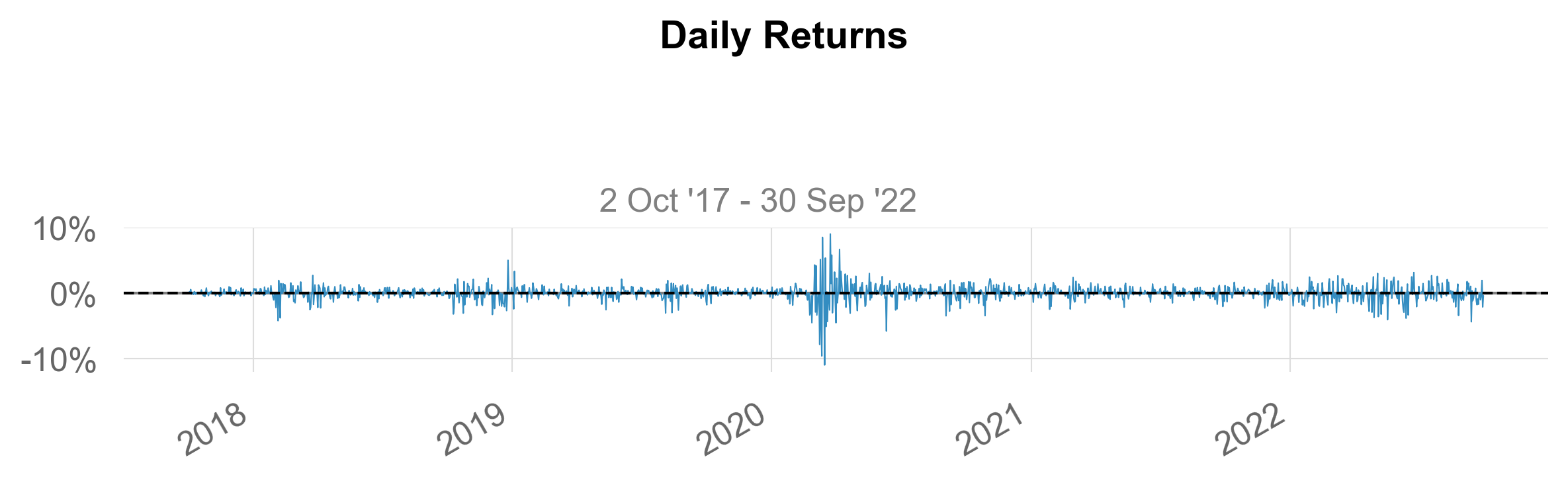

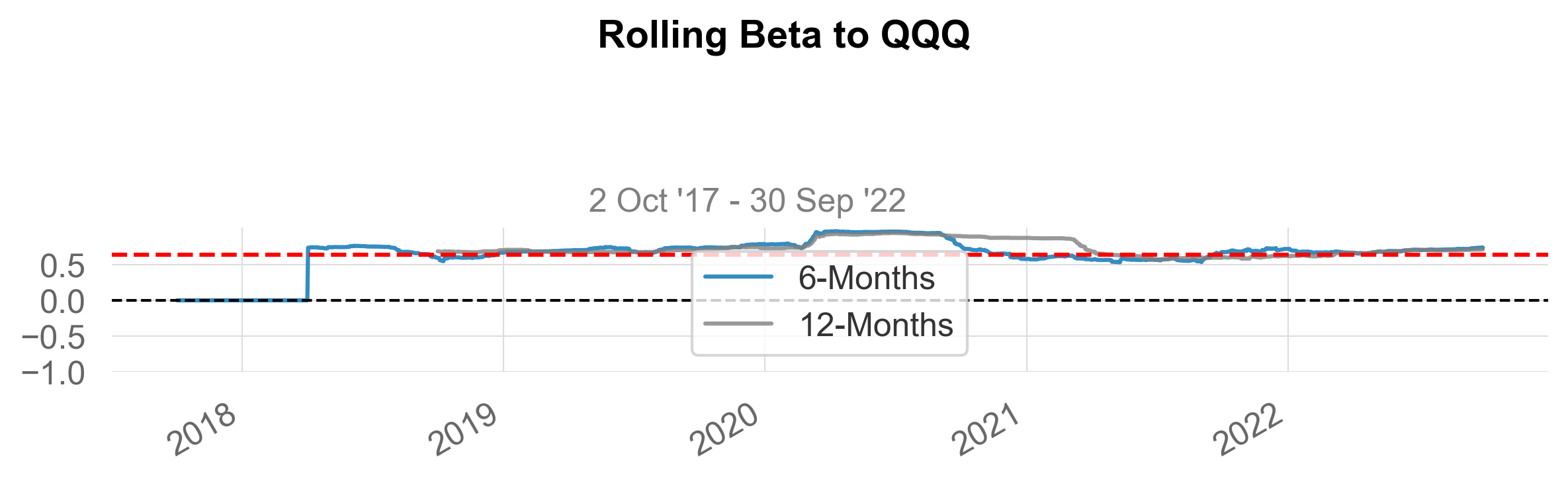

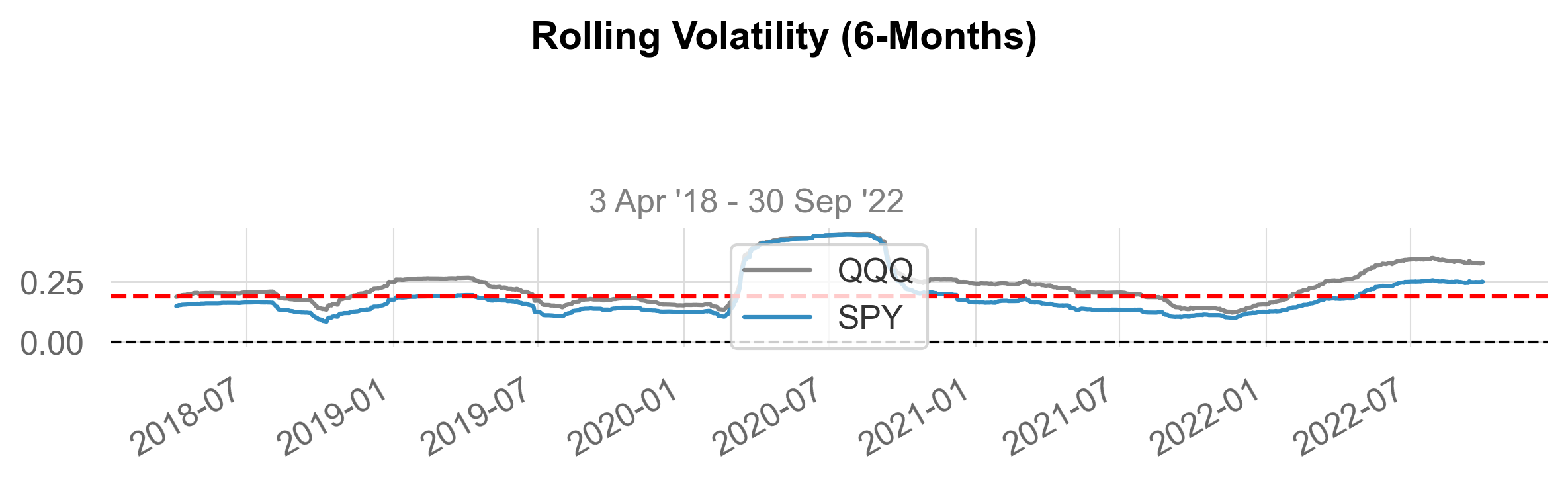

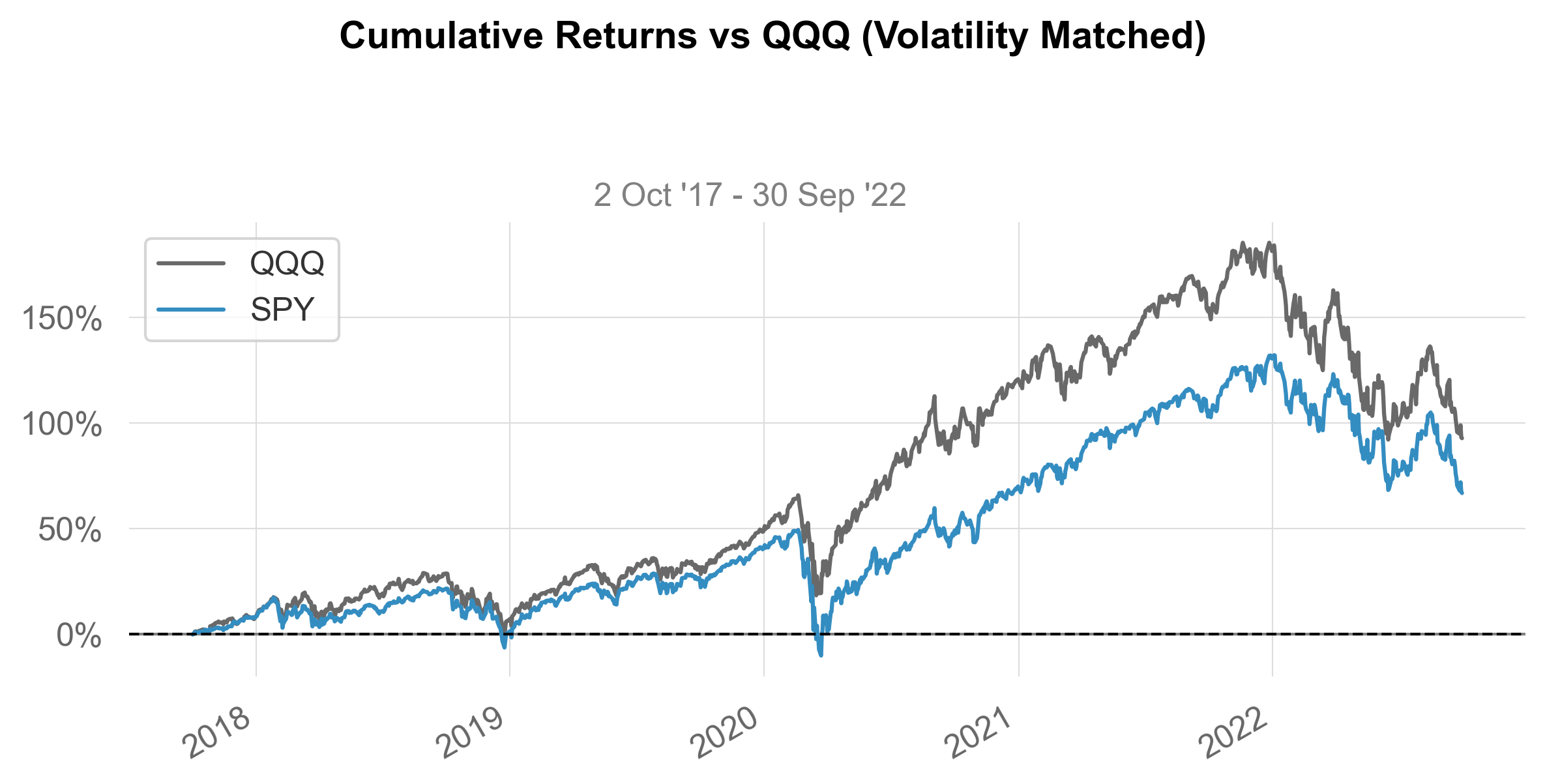

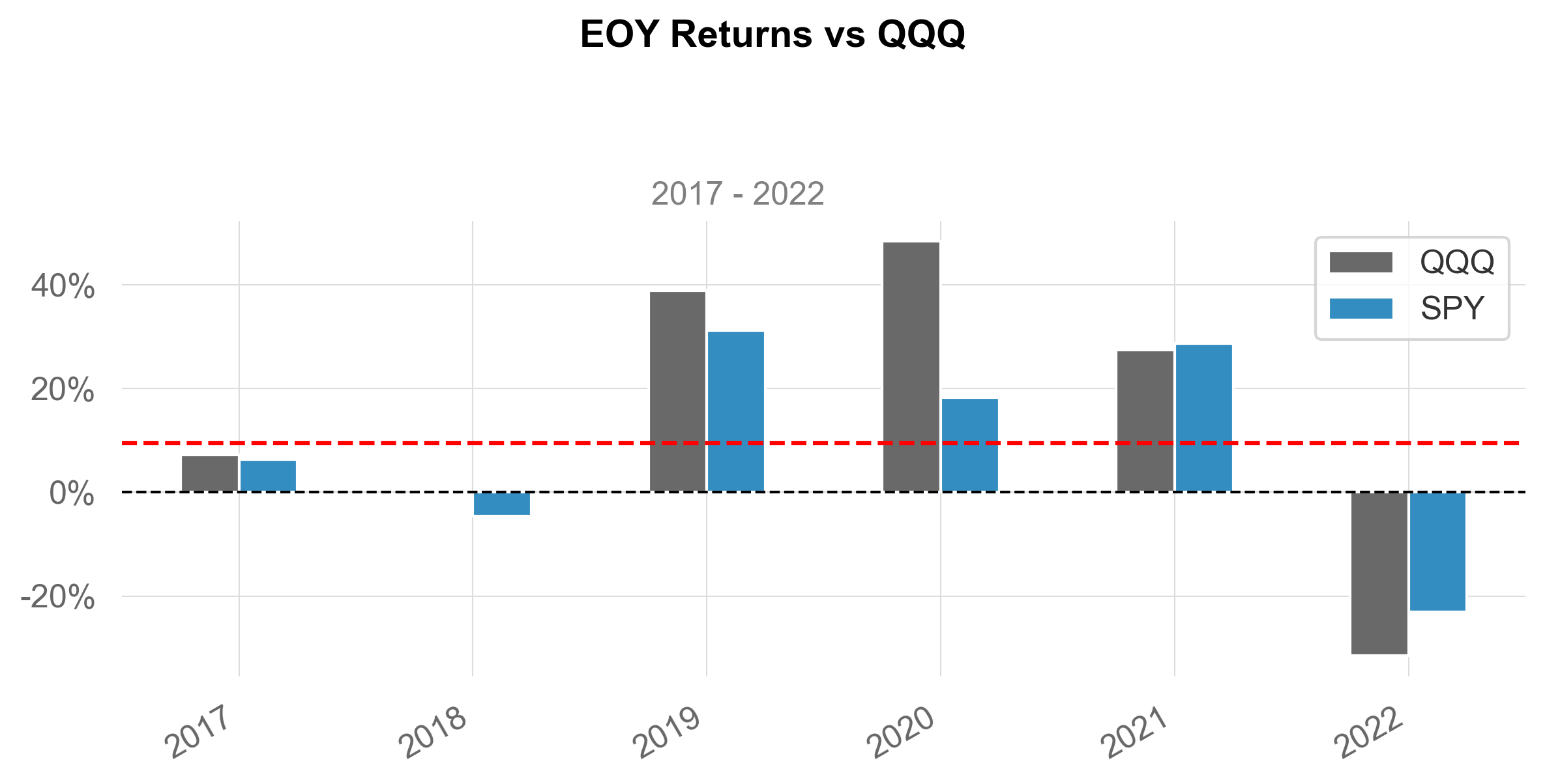

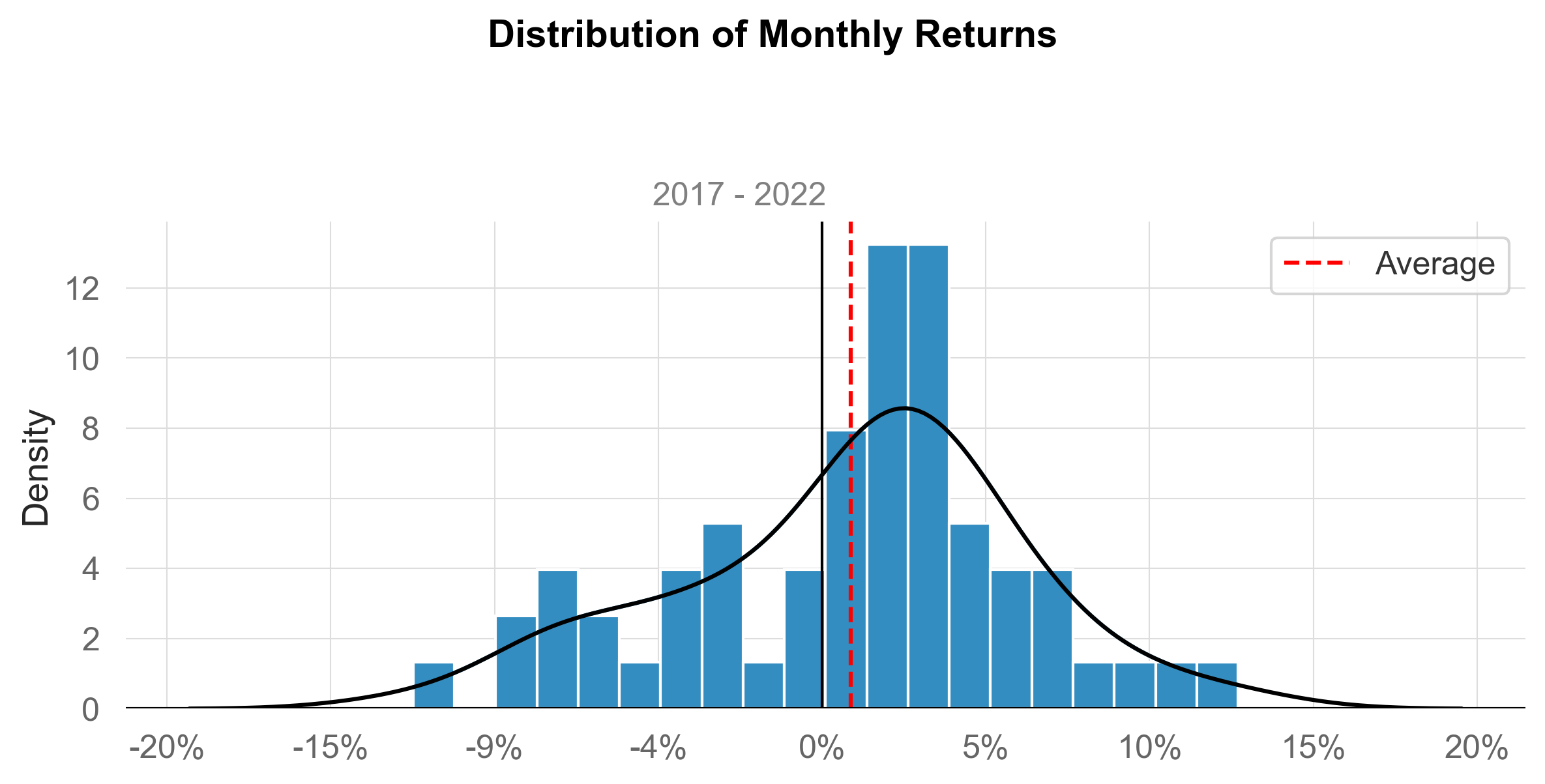

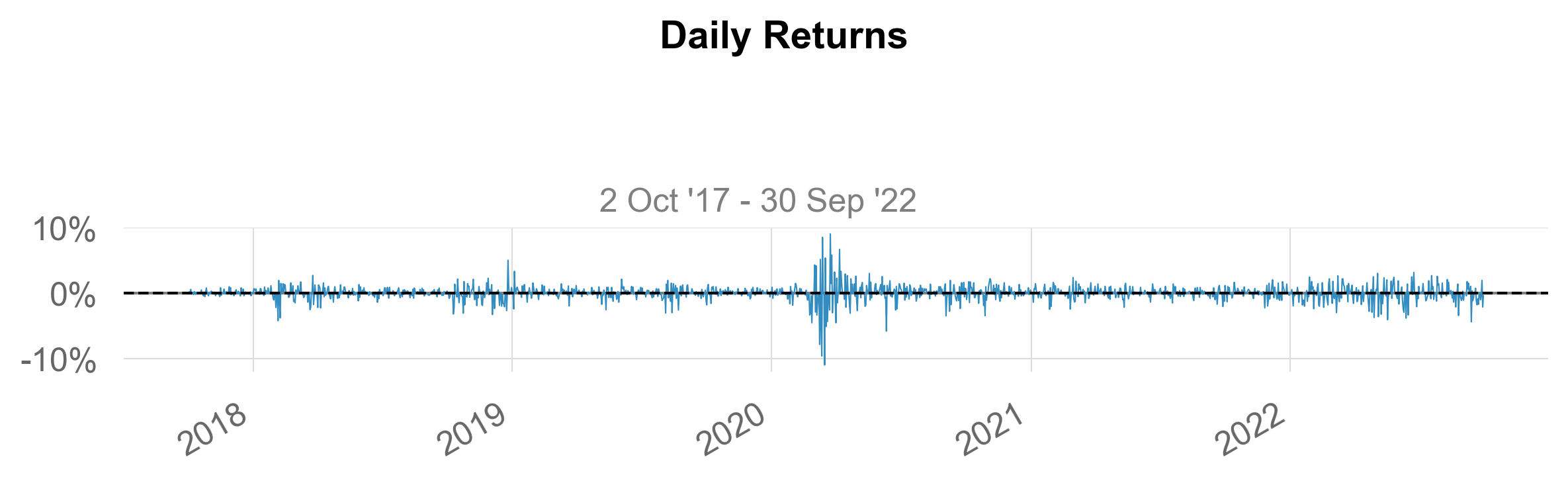

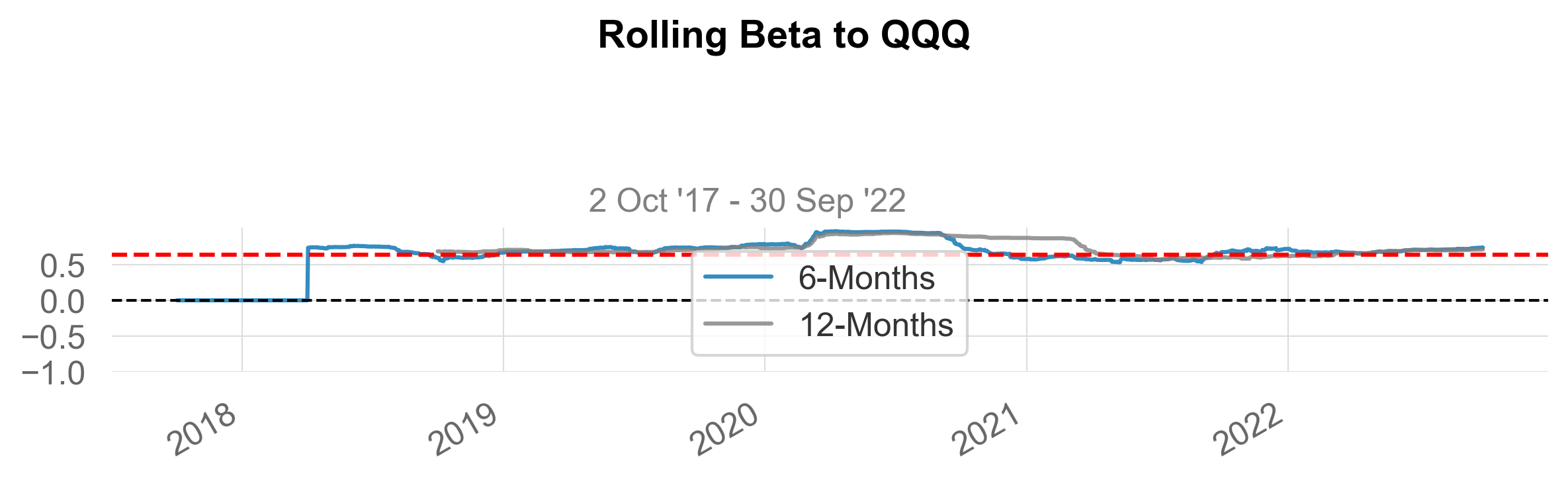

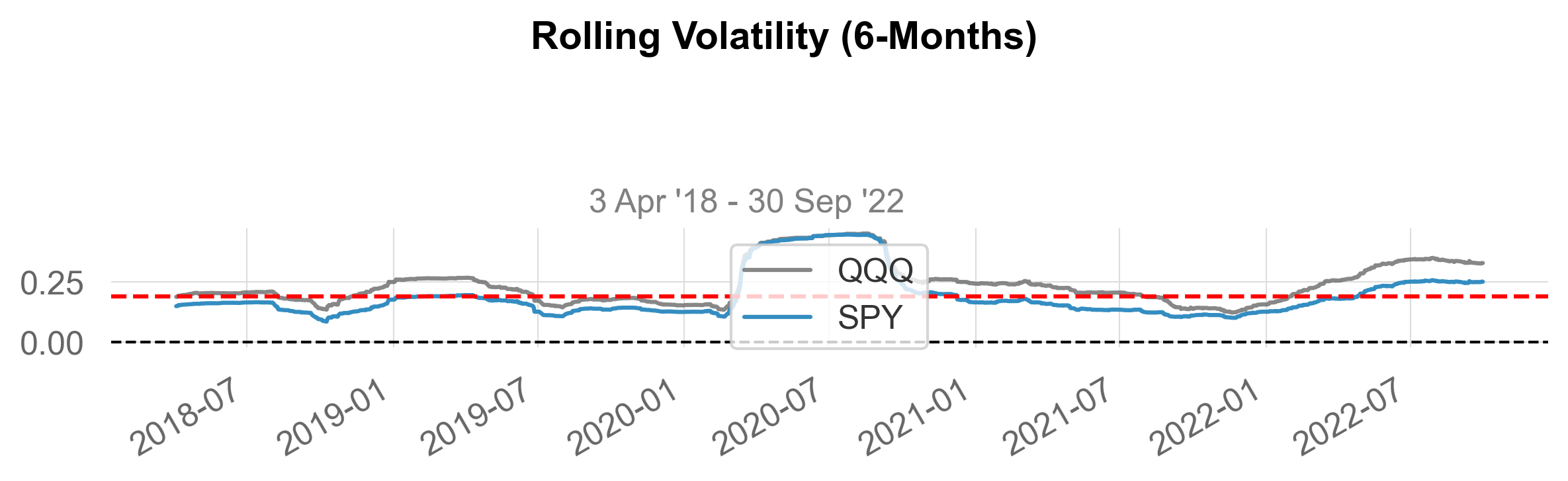

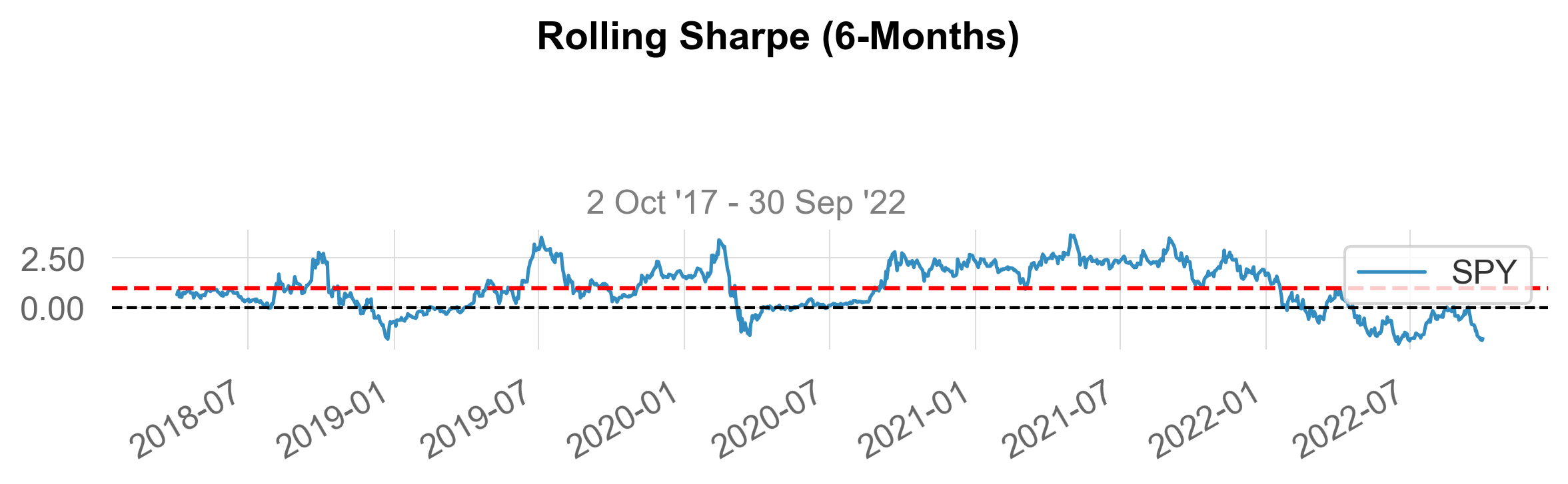

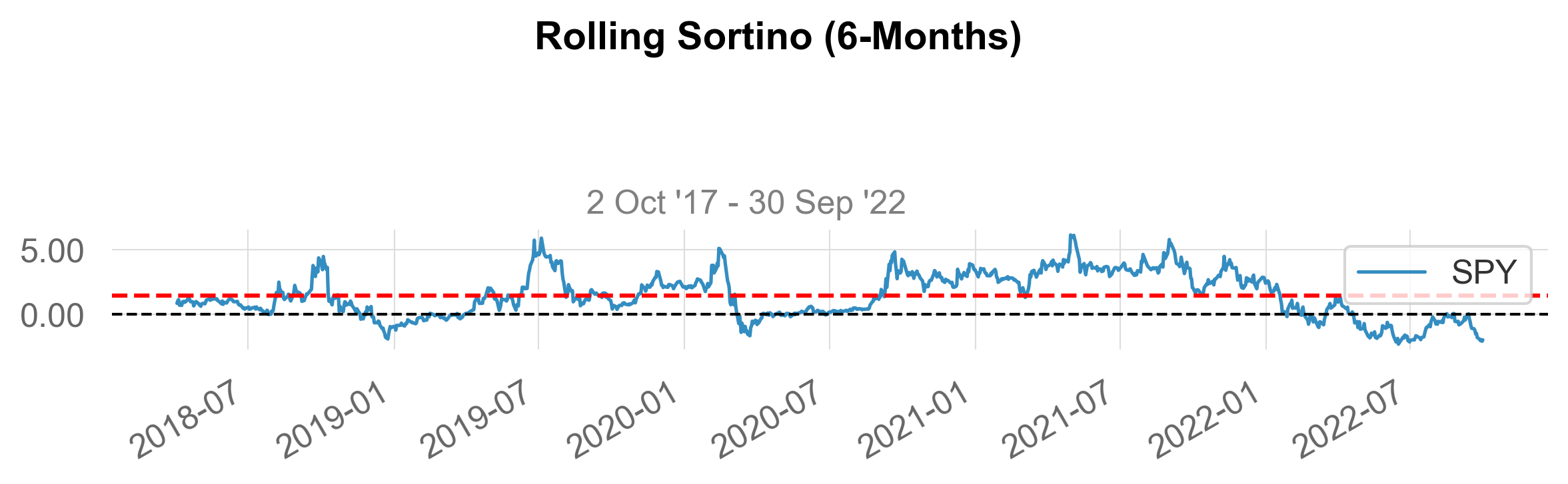

plots(returns, benchmark, returns_title = 'SPY', benchmark_title = 'QQQ', mode = 'full')

source

html

html (returns, benchmark=None, rf=0.0, grayscale=False, title='Strategy

Tearsheet', output=None, compounded=True, periods_per_year=252,

download_filename='quantstats-tearsheet.html', figfmt='svg',

template_path=None, match_dates=False, **kwargs)

Production of .html tearsheets

source

full

full (returns, benchmark=None, rf=0.0, grayscale=False, figsize=(8, 5),

display=True, compounded=True, periods_per_year=252,

match_dates=False, **kwargs)

returns = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

full(returns, benchmark, display=True, returns_title='SPY', benchmark_title='QQQ')

Performance Metrics

SPY QQQ

------------------------- ---------- ----------

Start Period 2017-10-02 2017-10-02

End Period 2022-09-30 2022-09-30

Risk-Free Rate 0.0% 0.0%

Time in Market 100.0% 100.0%

Cumulative Return 56.13% 92.85%

CAGR 9.32% 14.04%

Sharpe 0.53 0.65

Prob. Sharpe Ratio 88.02% 92.36%

Smart Sharpe 0.45 0.54

Sortino 0.73 0.89

Smart Sortino 0.61 0.75

Sortino/$\sqrt{2}$ 0.51 0.63

Smart Sortino/$\sqrt{2}$ 0.43 0.53

Omega 1.11 1.11

Max Drawdown -33.72% -32.65%

Longest DD Days 269 276

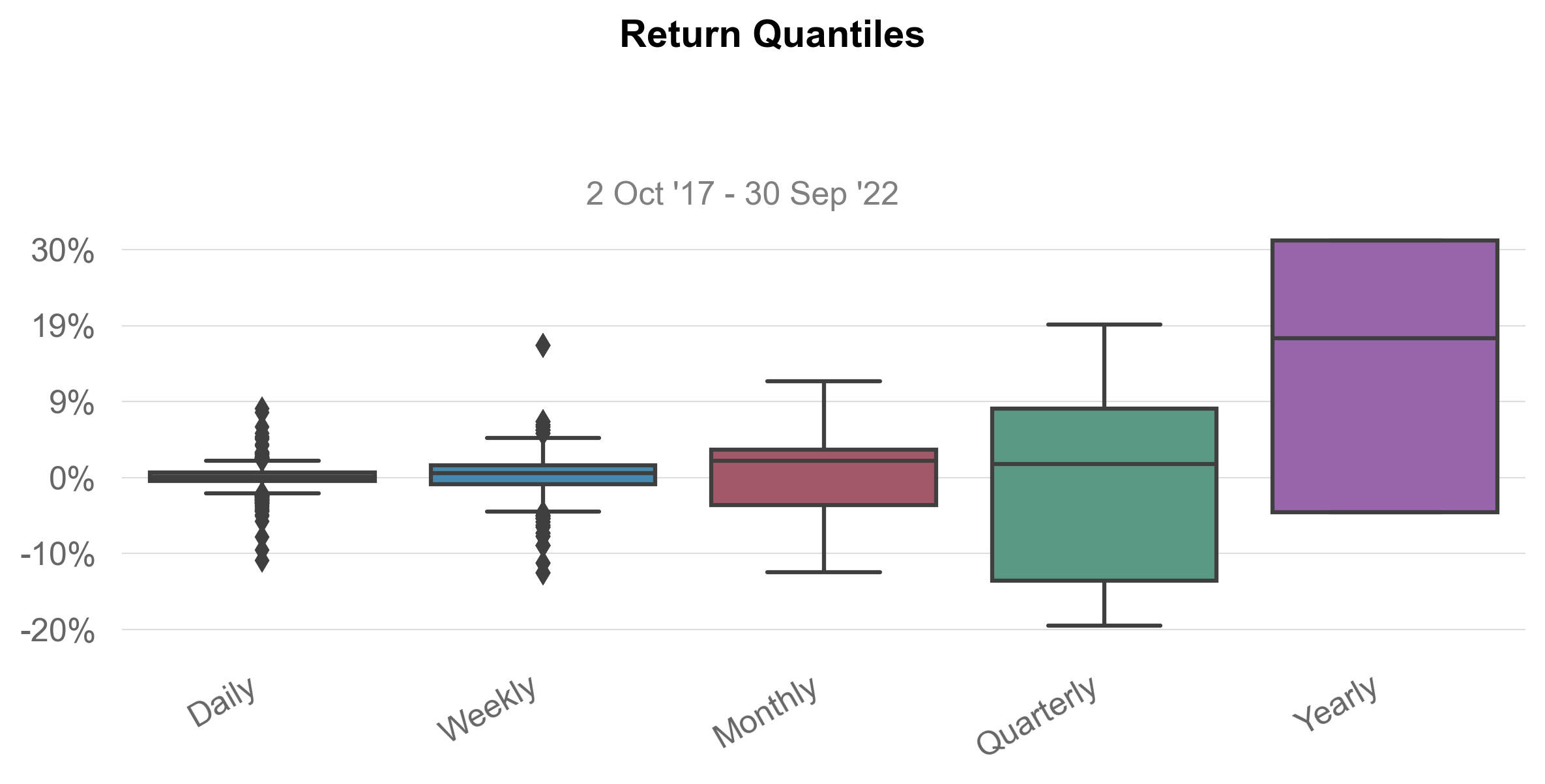

Volatility (ann.) 20.84% 25.29%

R^2 0.87 0.87

Information Ratio -0.03 -0.03

Calmar 0.28 0.43

Skew -0.66 -0.48

Kurtosis 12.01 5.9

Expected Daily % 0.04% 0.05%

Expected Monthly % 0.04% 0.05%

Expected Yearly % 0.04% 0.05%

Kelly Criterion 3.1% 5.27%

Risk of Ruin 0.0% 0.0%

Daily Value-at-Risk -2.11% -2.56%

Expected Shortfall (cVaR) -2.11% -2.56%

Max Consecutive Wins 11 11

Max Consecutive Losses 8 6

Gain/Pain Ratio 0.11 0.13

Gain/Pain (1M) 0.57 0.75

Payoff Ratio 0.85 0.85

Profit Factor 1.11 1.13

Common Sense Ratio 0.92 0.97

CPC Index 0.52 0.54

Tail Ratio 0.83 0.86

Outlier Win Ratio 4.46 3.47

Outlier Loss Ratio 4.57 3.45

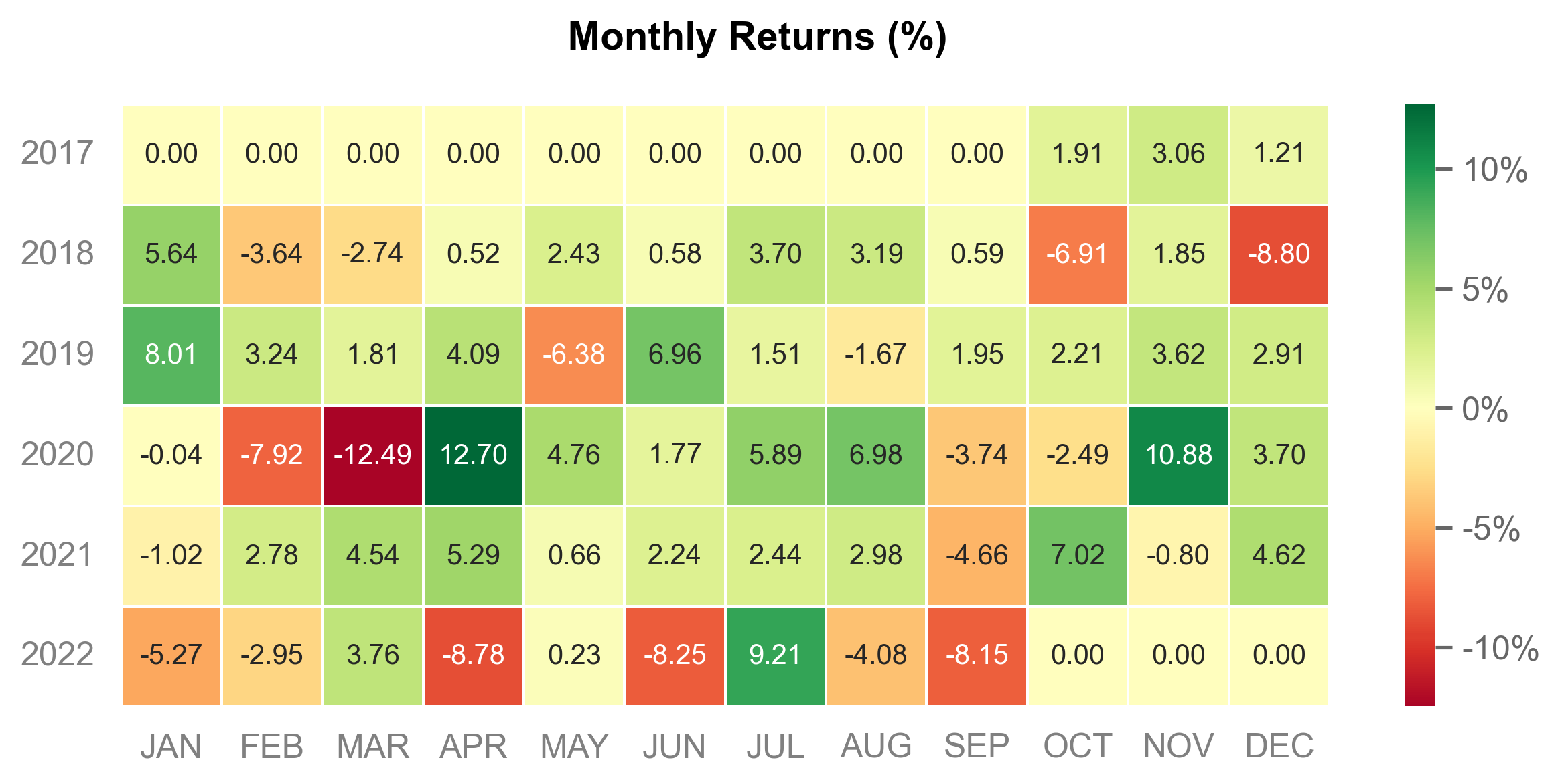

MTD -8.15% -9.18%

3M -4.56% -4.23%

6M -21.01% -26.63%

YTD -23.01% -31.46%

1Y -15.53% -24.01%

3Y (ann.) 7.97% 12.45%

5Y (ann.) 9.01% 13.4%

10Y (ann.) 9.32% 14.04%

All-time (ann.) 9.32% 14.04%

Best Day 9.06% 8.47%

Worst Day -10.94% -11.98%

Best Month 12.7% 14.97%

Worst Month -12.49% -13.6%

Best Year 31.22% 48.41%

Worst Year -23.01% -31.46%

Avg. Drawdown -1.92% -3.07%

Avg. Drawdown Days 16 19

Recovery Factor 1.66 2.84

Ulcer Index 0.08 0.1

Serenity Index 0.66 0.78

Avg. Up Month 4.21% 5.31%

Avg. Down Month -5.82% -6.51%

Win Days % 55.38% 56.48%

Win Month % 66.67% 63.33%

Win Quarter % 70.0% 75.0%

Win Year % 66.67% 66.67%

Beta 0.77 -

Alpha -0.01 -

Correlation 93.05% -

Treynor Ratio 73.22% -

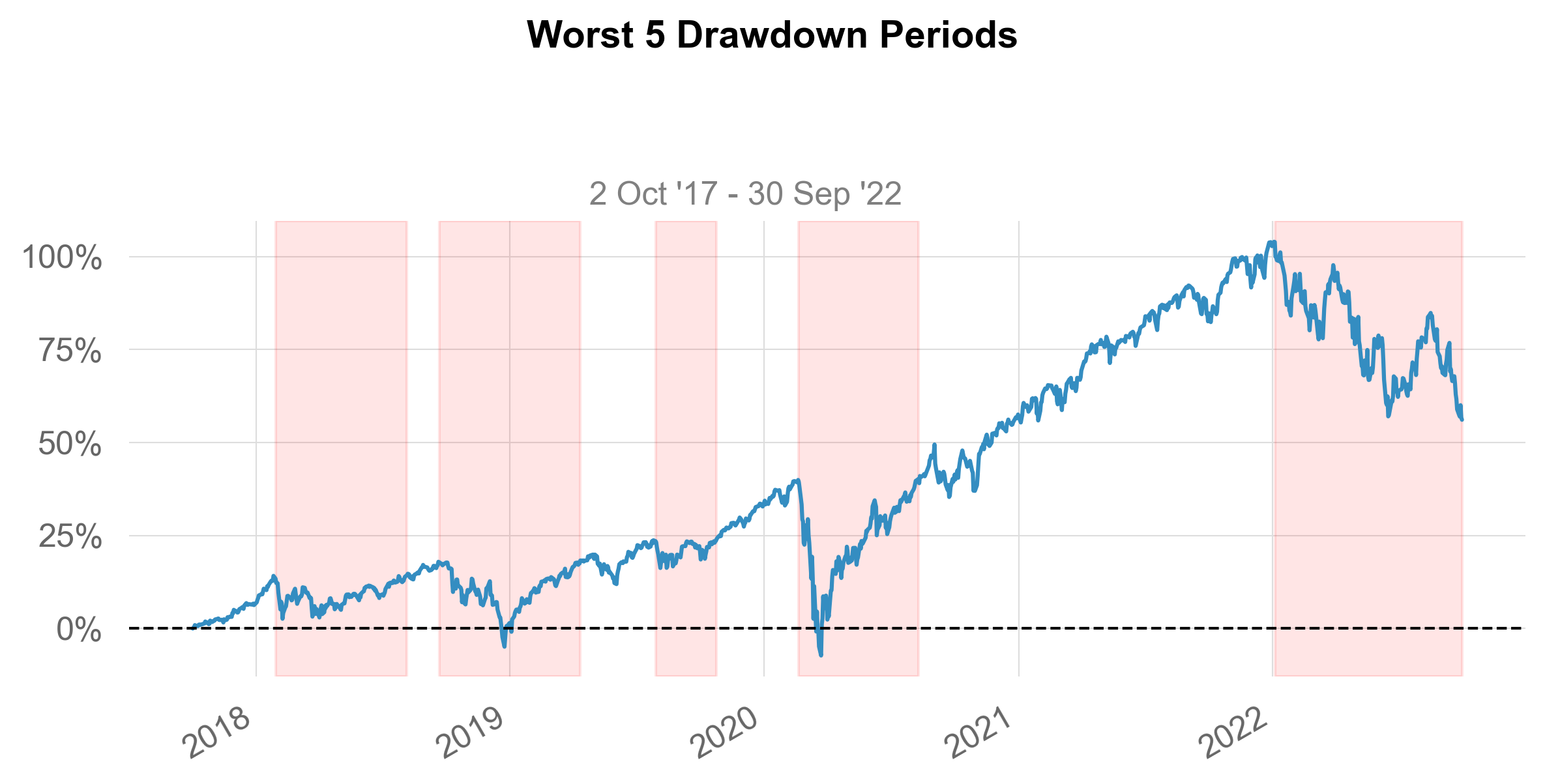

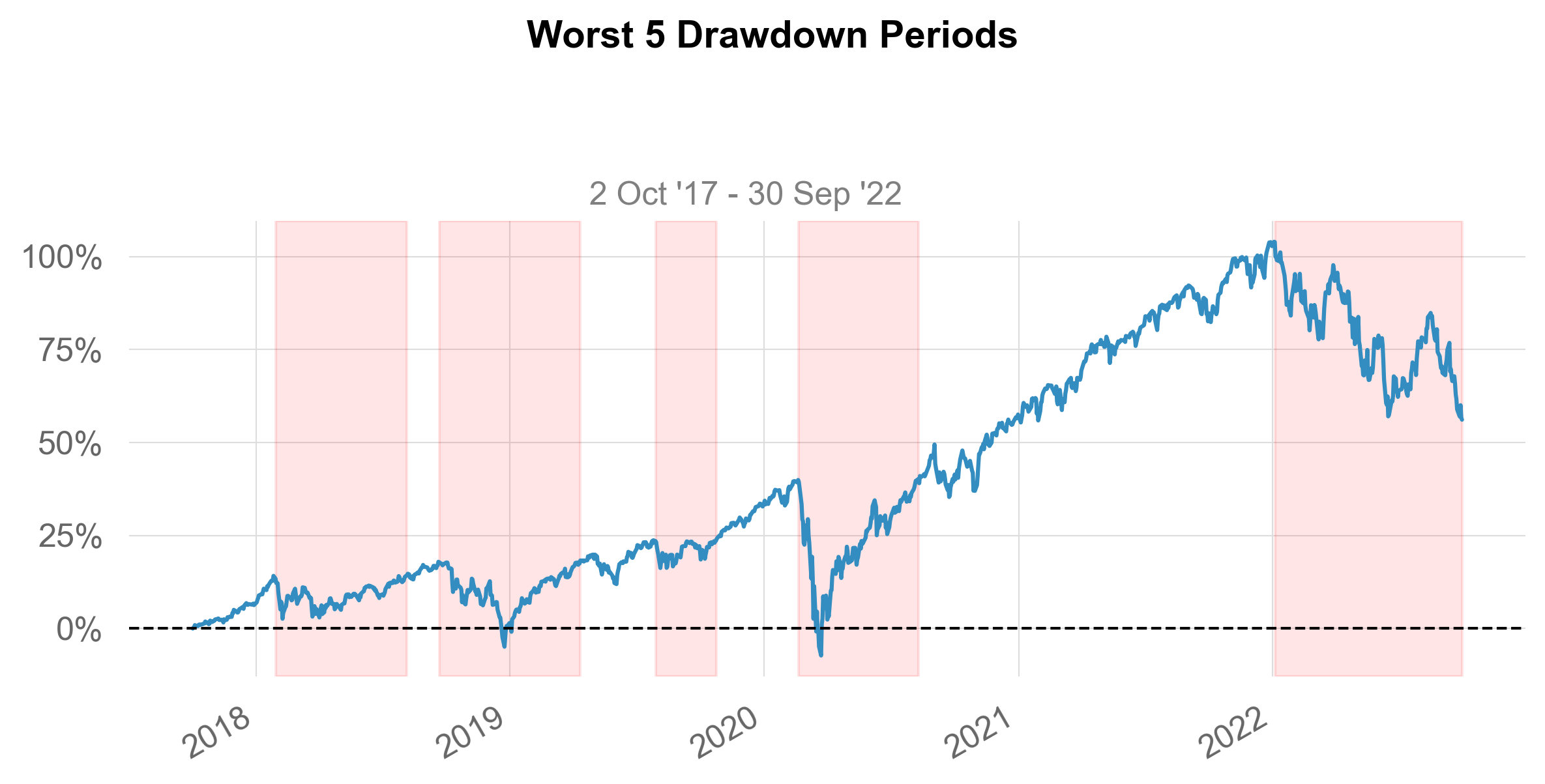

5 Worst Drawdowns

|

Start |

Valley |

End |

Days |

Max Drawdown |

99% Max Drawdown |

| 1 |

2020-02-20 |

2020-03-23 |

2020-08-10 |

172 |

-33.717262 |

-29.109770 |

| 2 |

2022-01-04 |

2022-09-30 |

2022-09-30 |

269 |

-23.448751 |

-23.052213 |

| 3 |

2018-09-21 |

2018-12-24 |

2019-04-12 |

203 |

-19.348908 |

-15.952035 |

| 4 |

2018-01-29 |

2018-02-08 |

2018-08-06 |

189 |

-10.101877 |

-9.594681 |

| 5 |

2020-09-03 |

2020-09-23 |

2020-11-11 |

69 |

-9.440438 |

-9.199067 |

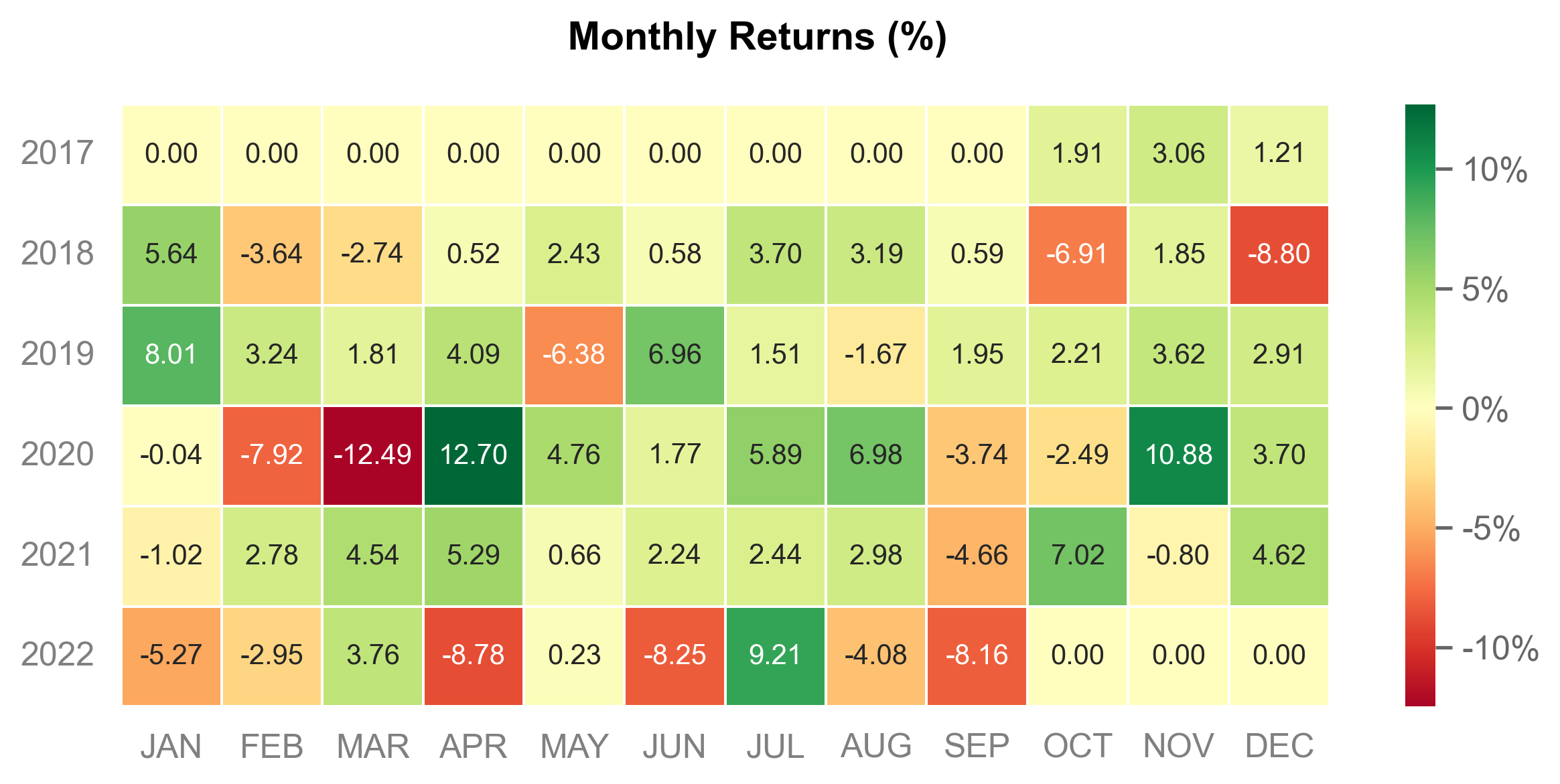

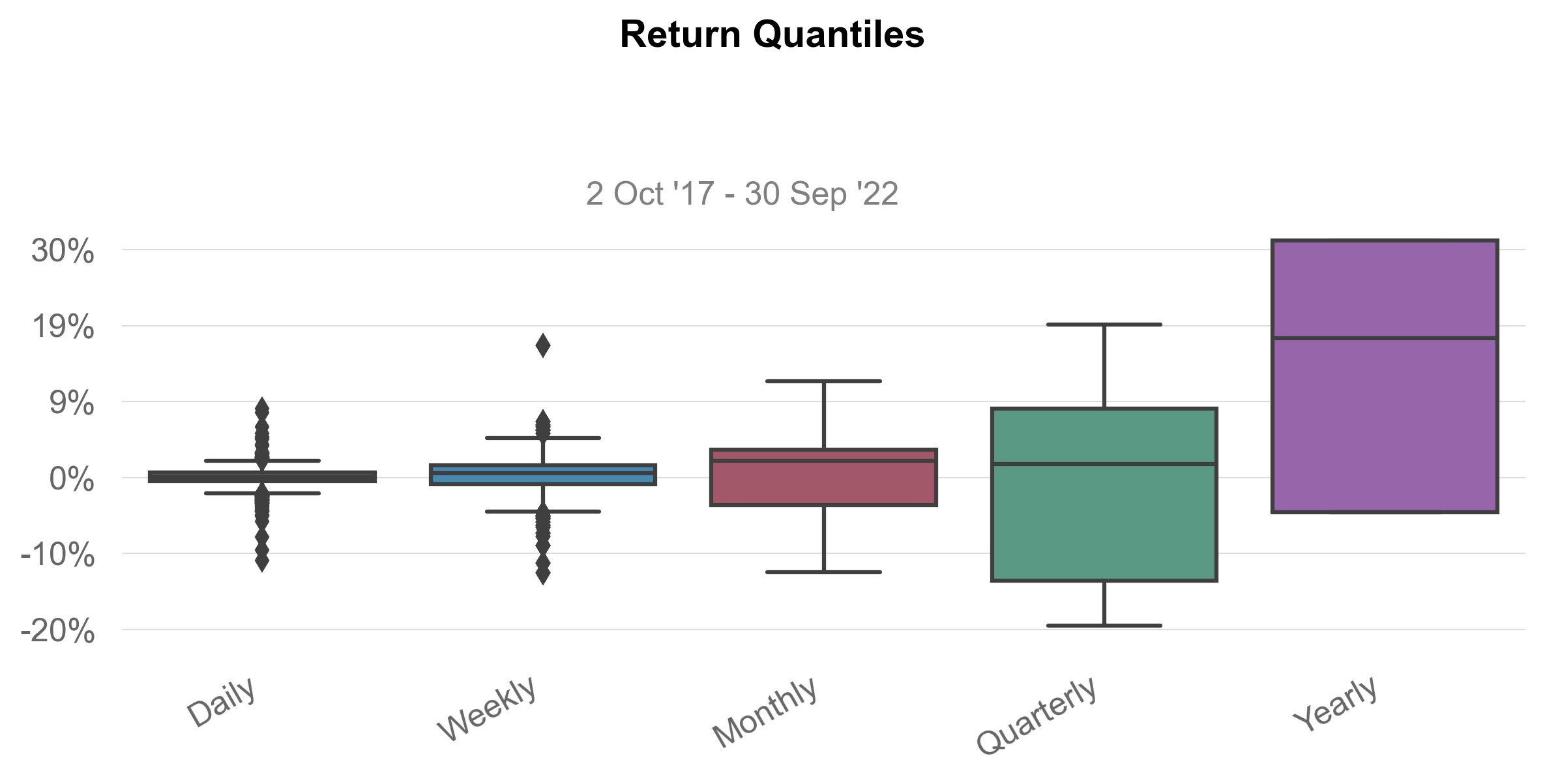

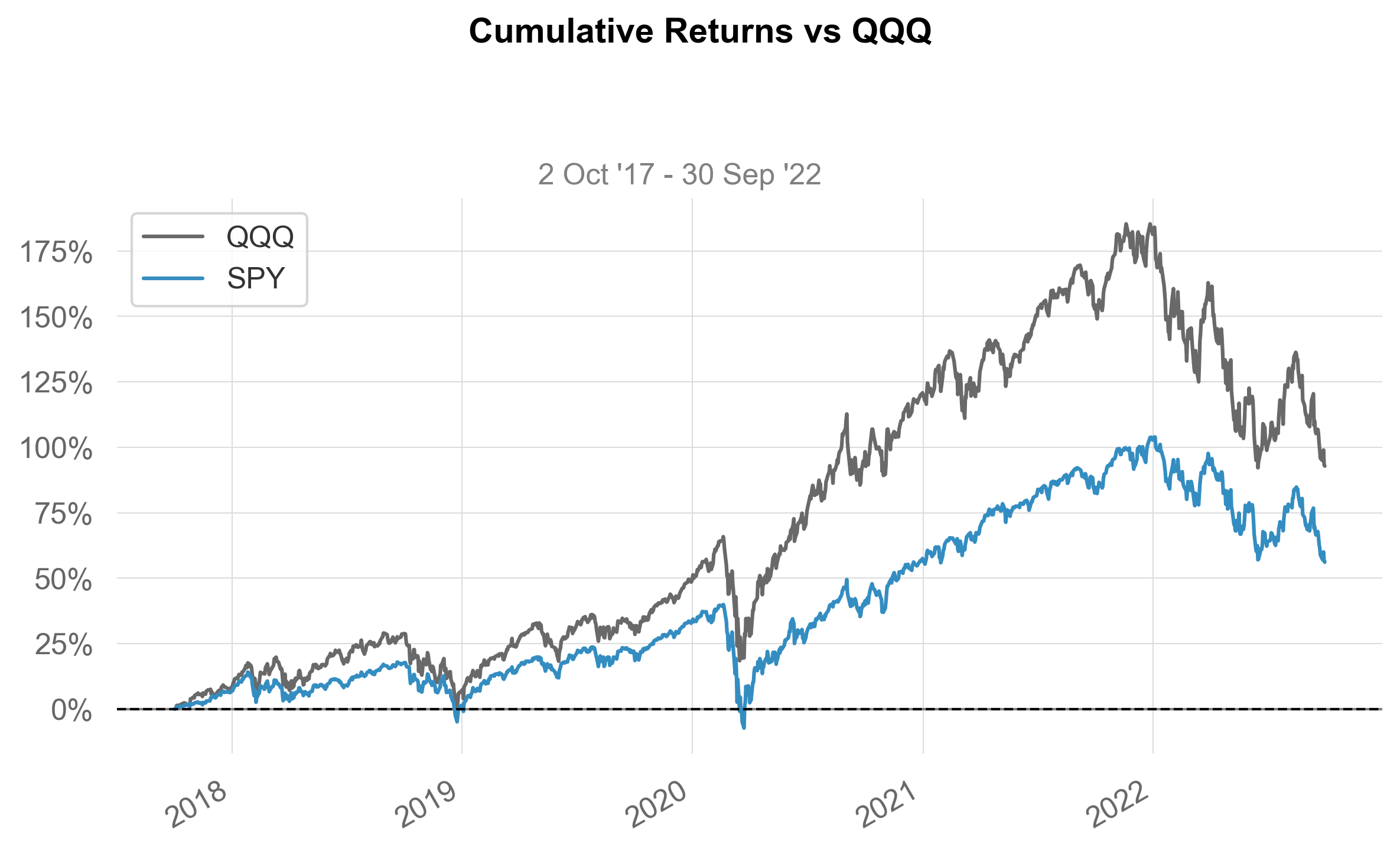

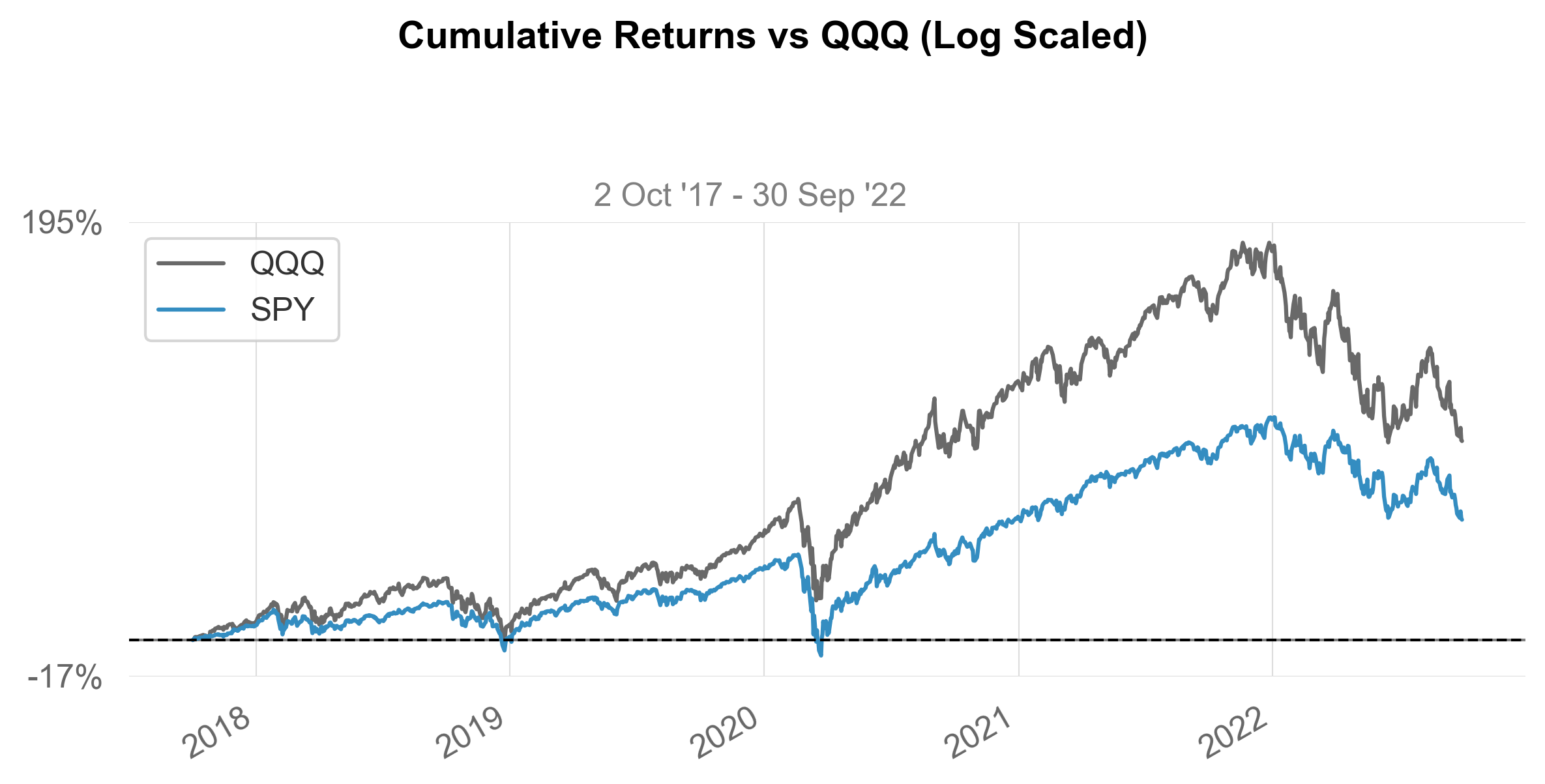

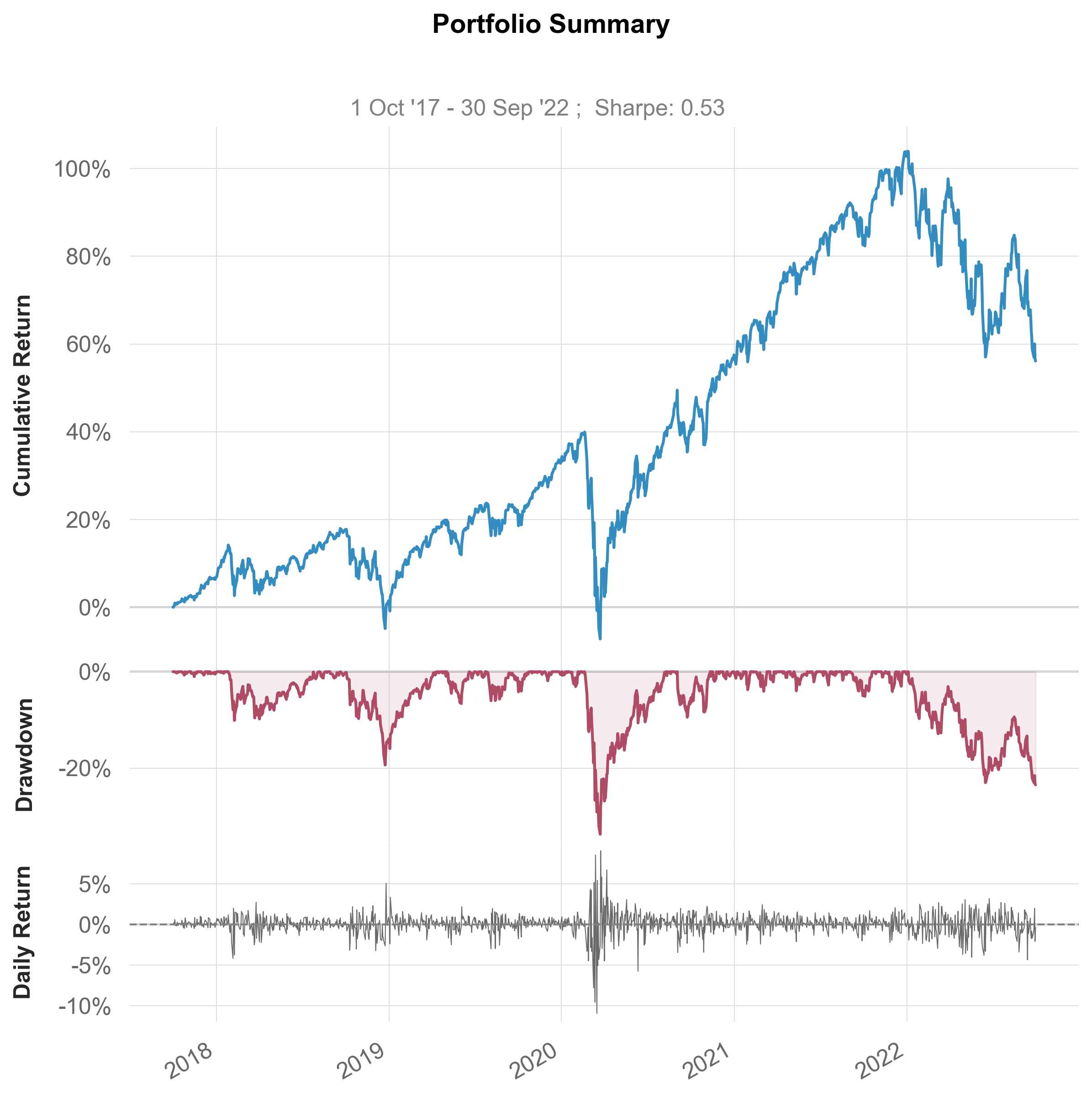

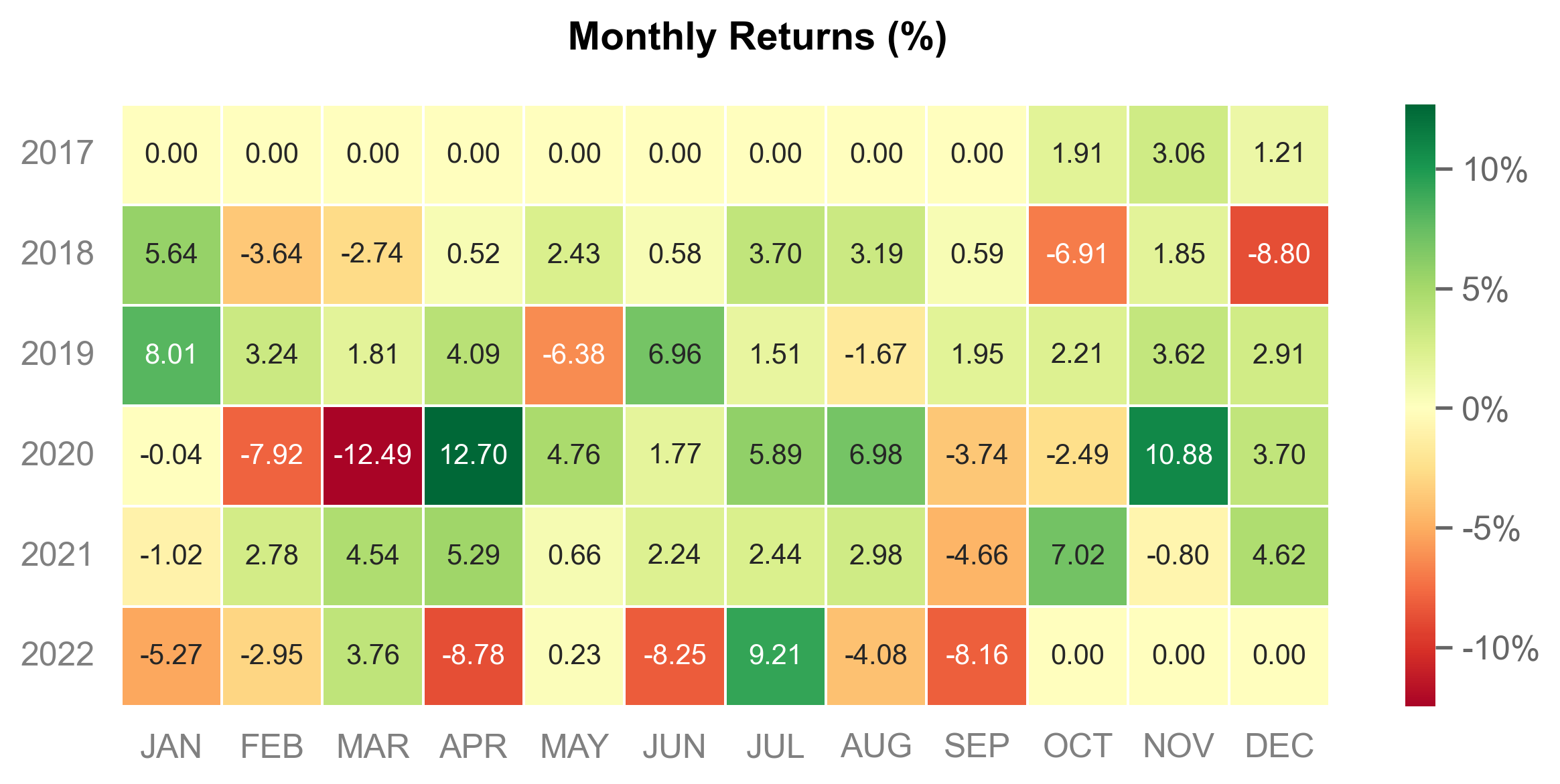

Strategy Visualization

source

basic

basic (returns, benchmark=None, rf=0.0, grayscale=False, figsize=(8, 5),

display=True, compounded=True, periods_per_year=252,

match_dates=False, **kwargs)

returns = _utils.download_returns('SPY', '5y')

benchmark = _utils.download_returns('QQQ', '5y')

basic(returns, benchmark, display=True)

Performance Metrics

Close Close

------------------ ---------- ----------

Start Period 2017-10-02 2017-10-02

End Period 2022-09-30 2022-09-30

Risk-Free Rate 0.0% 0.0%

Time in Market 100.0% 100.0%

Cumulative Return 56.11% 92.86%

CAGR 9.32% 14.05%

Sharpe 0.53 0.65

Prob. Sharpe Ratio 88.01% 92.37%

Sortino 0.73 0.89

Sortino/$\sqrt{2}$ 0.51 0.63

Omega 1.11 1.11

Max Drawdown -33.72% -32.65%

Longest DD Days 269 276

Gain/Pain Ratio 0.11 0.13

Gain/Pain (1M) 0.57 0.76

Payoff Ratio 0.85 0.85

Profit Factor 1.11 1.13

Common Sense Ratio 0.92 0.97

CPC Index 0.52 0.54

Tail Ratio 0.83 0.86

Outlier Win Ratio 4.46 3.47

Outlier Loss Ratio 4.57 3.45

MTD -8.16% -9.17%

3M -4.57% -4.22%

6M -21.02% -26.63%

YTD -23.02% -31.46%

1Y -15.54% -24.0%

3Y (ann.) 7.97% 12.45%

5Y (ann.) 9.0% 13.4%

10Y (ann.) 9.32% 14.05%

All-time (ann.) 9.32% 14.05%

Avg. Drawdown -1.92% -3.07%

Avg. Drawdown Days 16 19

Recovery Factor 1.66 2.84

Ulcer Index 0.08 0.1

Serenity Index 0.66 0.78

Strategy Visualization